Navigation

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

More options

Style variation

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

G20 Countries Economics Corner

- Thread starter Indos

- Start date

More options

Who Replied?

Indos

INT'L MOD

- Thread starter

- #2

Fed rate cuts triumph over Trump’s economic policies: A defining market battle

By

Amit Pabari

Last Updated: Nov 23, 2024, 01:13:00 PM IST

Synopsis

The Federal Reserve's rate cuts are poised to shape the U.S. and global economies, potentially overshadowing the impact of Donald Trump's economic policies. Despite short-term market fluctuations, the Fed's focus on stability and addressing fiscal challenges is expected to have a more lasting influence on markets, including the USD/INR, EUR/USD, and GBP/USD.

As the U.S. heads into a new political era following the 2024 presidential election, the financial markets are caught in a fierce tug-of-war between two monumental forces: the Federal Reserve’s ongoing rate cuts and Donald Trump’s potentially disruptive economic policies.

Despite the uncertainties surrounding Trump’s plans, the Fed’s methodical rate cuts appear to be the stronger contender in this market battle, likely defining economic trends well into 2025 and beyond.

The Fed’s Rate Cuts: The Key to Stability

Following a series of bold rate cuts—including a 50-basis-point reduction and a 25-basis-point cut in November 2024—the Federal Reserve remains committed to securing long-term economic stability.

The critical question now is whether the Fed will persist with its aggressive cuts or take a more cautious approach under external pressures, including Trump’s policies.

Several factors point to the likelihood of continued rate cuts:

1. Rising National Deficit

The Federal Reserve's current revenue stands at $3.27 trillion, while its spending has surged to $6.75 trillion, resulting in a significant deficit of $3.48 trillion. With the prospect of Trump returning to power, there are concerns that government spending will increase further, exacerbating the nation’s growing debt. This situation may necessitate a rate cut by the Fed to manage the fiscal imbalance. Additionally, it is striking that the U.S. government is now spending as much on interest payment as it does on critical sectors like defence, Medicare, and healthcare.

2. Soaring National Debt

The U.S. faces mounting fiscal challenges as national debt surpasses $35 trillion. Debt servicing costs are projected to exceed $1 trillion, prompting the Fed to continue rate cuts to ease borrowing costs. Meanwhile, consumer credit strains are intensifying, with credit card delinquencies hitting 8.8% and serious delinquencies (90+ days overdue) soaring to 11.1% in Q3 2024, the highest since 2011. Credit card debt has reached a record $1.17 trillion, leaving $130 billion at risk of default. These pressures underscore rising financial vulnerability among U.S. households.3. Bank Losses and Economic Strain

U.S. banks are under immense pressure, with losses on real estate debt securities soaring to $750 billion—seven times the losses seen during the 2008 crisis. Bank of America alone reported a staggering $116 billion in losses over the past three years. The strain on the financial system is palpable. If these challenges continue, the Fed will likely keep cutting rates to stabilize the banking sector, reduce borrowing costs, and prevent a collapse in the real estate market.4. Falling Household Savings

During the pandemic, Americans saved in record amounts, but by September 2024, households were $291 billion short of expected savings levels. This shortfall is creating a drag on consumer spending.

To combat this, the Fed will likely use rate cuts to stimulate demand, encouraging both spending and investment to prevent further economic slowdown.

Given these challenges, the Federal Reserve’s rate cuts seem set to continue into 2025. Their goal is clear: to stimulate growth, provide

relief to struggling borrowers, and maintain economic stability. Compared to Trump’s economic policies, the Fed’s approach appears more sustainable.

Trump’s Economic Policies: Short-Term Disruption, Long-Term Uncertainty

Trump’s economic policies—marked by aggressive tax cuts and tariffs—could initially create market excitement, but they are unlikely to overshadow the Fed’s rate cuts in the long run. While tax cuts could spur short-terminvestment and bolster the dollar, they come at a steep cost: a widening fiscal deficit and escalating national debt.

This could eventually erode confidence in the dollar, especially as the U.S. grapples with fiscal sustainability challenges. Trump’s trade policies, especially his tariffs on China, may further disrupt global trade relations, potentially triggering inflationary pressures and undermining the dollar’s value.

While the Dollar Index (DXY) may stay strong in the short term, its long-term outlook remains uncertain as trade tensions heighten and alternative currencies gain traction.

Moreover, historically, Trump has not been a champion of a strong dollar. During his presidency, the DXY dropped from 101.50 when he took office in 2017 to 88.12 by the end of 2018, and further to 90.58 when he left office in 2021.

This suggests his preference for a weaker dollar to stimulate exports. As the Fed continues to cut rates, Trump's policies could face growing challenges in supporting the dollar in the long term.

Technical Outlook –

On the technical front, the DXY is facing a strong resistance at the 0.5 Fibonacci retracement level around 107.16. A move below this level is expected to push the index toward 103.49. If this support is breached, it could open the door for a decline back to the 100 level.

Fed’s Victory: Shaping the USD/INR and Global Markets

The continued rate cuts by the Fed are beginning to reshape not only the U.S. economy but also global markets, including the USD/INR currency pair. While the dollar remains strong for now, ongoing monetary easing could eventually weaken the greenback, particularly if investors start questioning the the sustainability of U.S. fiscal policies.In India, the outflow of $14 billion from equities in October signals broader concerns about rising interest rates and inflation. However, as the Fed’s rate cuts take effect, there may be renewed interest in Indian equities, especially in sectors like information technology, defence, and clean energy.

These sectors, which saw growth during Trump’s first term, could experience a resurgence as investors seek better returns in emerging markets.

Despite the potential risks posed by Trump’s trade policies, India’s economic resilience remains strong. With a trade surplus of $54.7 billion in exports versus $28.5 billion in imports, the U.S.-India trade relationship remains a solid foundation.

Though tariffs may cause short-term disruption, the strategic partnership between the two nations is likely to continue fuelling growth, particularly in areas of mutual interest.

The USD/INR is expected to remain rangebound, likely trading between 83.80 and 84.50, with a slight bias toward the lower end. The interplay of these factors—Fed policy, Trump’s economic moves, and India’s resilient economy—will influence the currency pair in the coming months.

On the global stage, the EUR/USD and GBP/USD are finding robust support at 1.0450 and 1.2550, respectively. These levels are expected to act as springboards for upward movement, with EUR/USD eyeing 1.0800 and potentially reaching 1.10, while GBP/USD targets 1.2850 and possibly 1.3000 in the coming sessions.

(The author is MD, CR Forex Advisors)

Fed rate cuts triumph over Trump’s economic policies: A defining market battle

The Federal Reserve's rate cuts are poised to shape the U.S. and global economies, potentially overshadowing the impact of Donald Trump's economic policies. Despite short-term market fluctuations, the Fed's focus on stability and addressing fiscal challenges is expected to have a more lasting...

Last edited:

Indos

INT'L MOD

- Thread starter

- #3

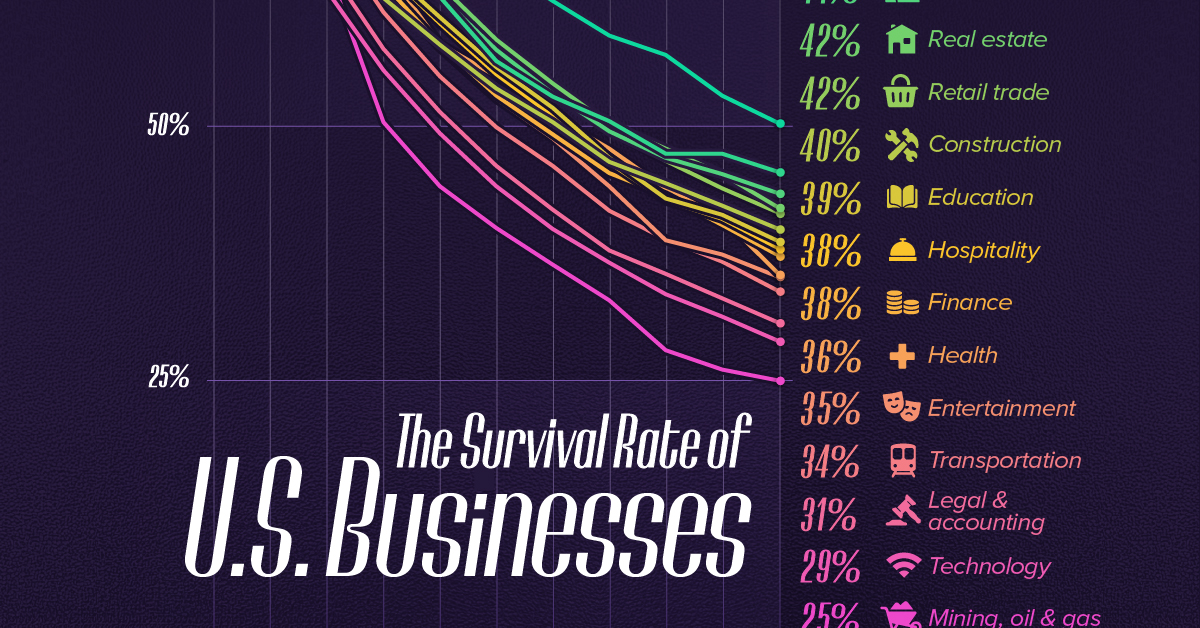

Charted: The Survival Rate of U.S. Businesses (2013-2023)

Published

November 19, 2024 By Pallavi Rao

Only 34.7% of Businesses Survived Between 2013 and 2023

During the pandemic a record number of Americans turned entrepreneurs—sending new business applications to soaring heights.

But everyone knows running a business is difficult, and now there’s some new data to validate the sentiment.

This chart tracks the survival rate of all private American companies born in 2013, categorized by industry. Figures for this chart are rounded and sourced from the Bureau of Labor Statistics (BLS), published 2024.

How Hard is it to Run a Business in America?

Unsurprisingly survival rates for new businesses depend on the industry they’re operating in.

From the data, Agriculture and Forestry businesses born in 2013 were the most resilient over the last decade. More than half were still in operation by 2023.

Note: Only select years shown and industry labels lightly modified, both for readability.

In stark contrast, only one-fourth of Mining, Oil & Gas firms survived in the same time period.

Interestingly both industries are some of the largest subsidy receivers from the government. Estimates put federal agricultural support at $30 billion annually—heavily subsidizing five major crops: corn, soybeans, wheat, cotton, and rice.

Meanwhile, the American energy sector receives about $20 billion a year, 80% of which goes to oil and gas.

It is possible that differences in ownership structure and business size are contributing to wildly different survival rates. For example, 97% of all U.S. farms are still family-owned and 88% of them are “small farms” which may need less capital investment than an oil & gas business.

One trend that is industry-agnostic is that the first year proved the most brutal for all businesses formed in 2013, with a 20 percentage point decline in survivors. As time passed, the declines continued at a slower rate.

Finally, the BLS found that for all private businesses incorporated in 2013, just over one-third (34.7%) were still functioning in 2023.

Charted: How Many U.S. Firms Born in 2013 Made It to 2023

Business survival rates depend on the industry they’re in. Here’s how companies born in 2013 have done so far.

Indos

INT'L MOD

- Thread starter

- #4

How A Second Trump Presidency Will Impact Indonesian Economy

Lili Yan Ing, Yessi Vadilla

November 18, 2024 | 1:59 am With Donald Trump’s return to the White House, we are likely to witness a renewed focus on the "America First" policy, which emphasizes reshoring jobs, reducing trade deficits, and tightening immigration policies. Such a stance holds significant implications for emerging economies like Indonesia. Here, we explore the anticipated impacts of Trump’s potential economic policies on the Indonesian economy from 2024 to 2029, specifically in relation to tariffs and trade deficits, the generalized system of preferences (GSP), global supply chain reorientation, and foreign direct investment (FDI).

First, Tariffs and Trade Deficits. During his previous term, Trump employed aggressive tariffs to reduce the US trade deficit, particularly targeting imports from China. In his current term, he has expressed intentions to impose tariffs as high as 60 percent on Chinese imports (and up to 200 percent on electric vehicles), with potential 10-20 percent tariffs on imports from other countries. Such measures could have both direct and indirect repercussions for Indonesia.

Directly, Indonesia stands as one of the United States' largest Southeast Asian trading partners after Vietnam, exporting products like palm oil, electronic components, machinery, textiles, footwear, tires, and rubber. In 2023, Indonesia’s exports to the US were valued at $23.3 billion, largely comprised of inputs and raw materials for US production. Increased tariffs on ASEAN countries would raise costs for these products, making Indonesian goods more expensive for US producers and consumers, which could ultimately erode US manufacturing competitiveness and contribute to inflationary pressures.

Indirectly, any escalation of the US-China trade war -- which has extended to encompass technology, strategic industries, and national security -- would have regional implications, particularly for Southeast Asia. Indonesia, integrated within East Asian supply chains, could be adversely affected if demand decreases for inputs and intermediate goods essential to broader production networks.

Second, the Generalized System of Preferences (GSP). The GSP program, established in 1976, provides duty-free access to the US market for select goods from developing countries. This preferential treatment benefits Indonesian exports of electronic equipment, travel goods, chemicals, furniture, and rubber. In 2023, Indonesia exported $3.56 billion under GSP.

Trump’s administration previously removed countries like India and Turkey from GSP eligibility, citing trade imbalances and other concerns. Indonesia has undergone GSP eligibility reviews before, most recently in 2017, as part of the US Trade Representative’s “proactive” process. If Trump reconsiders Indonesia’s GSP status, a suspension or termination of these preferences could increase costs for U.S. companies reliant on Indonesian goods, reducing their competitiveness in global markets and potentially decreasing Indonesia’s exports to the US.

Third, Global Supply Chain Reorientation. Another core aim of Trump’s economic approach is reshoring manufacturing jobs to the US, reducing reliance on foreign suppliers. This strategy could impact Indonesia’s manufacturing sector, particularly as it relates to electronics and automotive production, where Indonesia has benefited from global production sharing.

A shift away from Asian supply chains may result in decreased manufacturing demand for Indonesian industries, potentially lowering output and exports in key sectors. However, Indonesia could also benefit from a “China Plus One” strategy, where firms seek alternatives to China but maintain part of their operations in nearby countries. Indonesia’s competitive labor costs, large domestic market, and advantageous position within ASEAN make it an attractive alternative manufacturing hub, albeit with some infrastructure and regulatory challenges.

Fourth, Foreign Direct Investment (FDI). During his previous term, he introduced tax cuts and regulatory incentives designed to encourage US companies to invest domestically. Should a similar approach be implemented in his second term, it could affect US FDI flows to Indonesia. In 2023, FDI from the US into Indonesia totaled $3.3 billion, representing 6.5 percent of total FDI inflows, placing the US fifth after ASEAN, China, Hong Kong, and Japan. US FDI has traditionally been concentrated in sectors such as finance (notably banking and insurance), mining, energy, and consumer goods.

Concerns exist that Trump’s tax policies could lead to a decline in US FDI abroad if American companies are encouraged to reinvest earnings domestically. Such a shift would impact Indonesian industries reliant on U.S. capital, technology, and expertise.

In conclusion, a second Trump administration presents both challenges and potential opportunities for Indonesia’s economy. The possibility of heightened tariffs, a GSP review, and a push toward US supply chain reshoring could disrupt trade relations, reduce investment, and require Indonesia to adapt diplomatically and economically.

Mitigating these risks will require Indonesia to diversify its economic partnerships, strengthen local manufacturing, and build trade ties with other major economies to lessen reliance on any single market. Moreover, Indonesia must explore new sources of FDI, potentially increasing investment from China, Japan, South Korea, and the Middle East to compensate for any declines from the US.

By building resilience through regional alliances and establishing a robust ASEAN presence, Indonesia can weather shifts in US economic policy and maintain steady growth in an increasingly multipolar world.

---

Lili Yan Ing is the Secretary General of the International Economic Association (IEA). Yessi Vadila is the Trade Specialist at the Economic Research Institute for ASEAN and East Asia (ERIA).

How A Second Trump Presidency Will Impact Indonesian Economy

A shift away from Asian supply chains may result in decreased manufacturing demand for Indonesian industries.

Indos

INT'L MOD

- Thread starter

- #5

Is the fastest-growing big economy losing steam?

10 hours ago

Between July and September, India's economy slumped to a seven-quarter low of 5.4%

Soutik Biswas

India correspondent•@soutik

BBC

Is the world's fastest-growing big economy losing steam?

The latest GDP numbers paint a sobering picture. Between July and September, India's economy slumped to a seven-quarter low of 5.4%, well below the Reserve Bank of India (RBI) forecast of 7%.

While it is still robust compared with developed nations, the figure signals a slowdown.

Economists attribute this to several factors. Consumer demand has weakened, private investment has been sluggish for years and government spending - an essential driver in recent years - has been pulled back. India's goods exports have long struggled, with their global share standing at a mere 2% in 2023.

Fast-moving consumer goods (FMCG) companies report tepid sales, while salary bills at publicly traded firms, a proxy for urban wages, shrank last quarter. Even the previously bullish RBI has revised its growth forecast to 6.6% for the financial year 2024-2025.

"All hell seems to have broken loose after the latest GDP numbers," says economist Rajeshwari Sengupta. "But this has been building up for a while. There's a clear slowdown and a serious demand problem."

Finance Minister Nirmala Sitharaman paints a brighter picture. She said last week that the decline was "not systemic" but a result of reducing government spending during an election-focused quarter. She expected third-quarter growth to offset the recent decline. India will probably remain the fastest-growing major economy despite challenges like stagnant wages affecting domestic consumption, slowing global demand and climate disruptions in agriculture, Sitharaman said.

India's inflation surged to 6.2% in October, mainly driven by high vegetable prices

Some – including a senior minister in the federal government, economists and a former member of RBI's monetary policy group – argue that the central bank's focus on curbing inflation has led to excessively restrictive interest rates, potentially stifling growth.

High rates make borrowing more expensive for businesses and consumers, and potentially reduce investments and dampen consumption, both key drivers of economic growth. The RBI has kept interest rates unchanged for nearly two years, primarily because of rising inflation.

India's inflation surged to 6.2% in October, breaching the central bank's target ceiling (4%) and reaching a 14-month high, according to official data. It was mainly driven by food prices, comprising half of the consumer price basket – vegetable prices, for example, rose to more than 40% in October. There are also growing signs that food price hikes are now influencing other everyday costs, or core inflation.

But high interest rates alone may not fully explain the slowing growth. "Lowering rates won't spur growth unless consumption demand is strong. Investors borrow and invest only when demand exists, and that's not the case now," says Himanshu, a development economist at Delhi's Jawaharlal Nehru University.

However, RBI's outgoing governor, Shaktikanta Das, believes India's "growth story remains intact", adding the "balance between inflation and growth is well poised".

Economists point out that despite record-high retail credit and rising unsecured loans - indicating people borrowing to finance consumption even amidst high rates - urban demand is weakening. Rural demand is a brighter spot, benefiting from a good monsoon and higher food prices.

India's central bank has kept interest rates unchanged for nearly two years, citing inflation risks

Ms Sengupta, an associate professor at Mumbai-based Indira Gandhi Institute of Development Research, told the BBC that the ongoing crisis was borne out by the fact that India's economy was operating on a "two-speed trajectory", driven by diverging performances in its "old economy and new economy".

The old economy comprising the vast informal sector, including medium and small scale industries, agriculture and traditional corporate sector, are still waiting for long-pending reforms.

In contrast, the new economy, defined by the boom in services exports post-Covid, experienced robust growth in 2022-23. Outsourcing 2.0 has been a key driver, with India emerging as the world's largest hub for global capability centres (GCCs), which do high-end offshore services work.

According to Deloitte, a consulting firm, over 50% of the world's GCCs are now based in India. These centres focus on R&D, engineering design and consulting services, generating $46bn (£36bn) in revenue and employing up to 2 million highly skilled workers.

"This influx of GCCs fuelled urban consumption by supporting demand for luxury goods, real estate and SUVs. For 2-2.5 years post-pandemic, this drove a surge in urban spending. With GCCs largely established and consumption patterns shifting, the urban spending lift is fading," says Ms Sengupta.

So the old economy appears to lack a growth catalyst while the new economy slows. Private investment is crucial, but without strong consumption demand, firms will not invest. Without investment to create jobs and boost incomes, consumption demand cannot recover. "It's a vicious cycle," says Ms Sengupta.

There are other confusing signals as well. India's average tariffs have risen from 5% in 2013-14 to 17% now, higher than Asian peers trading with the US. In a world of global value chains, where exporters rely on imports from multiple countries, high tariffs make goods more expensive for companies to trade, making it harder for them to compete in global markets.

Car sales have dropped by 14% in November - another signal of weakening demand

Then there is what economist Arvind Subramanian calls a "new twist in the tale".

Even as calls grow to lower interest rates and boost liquidity, the central bank is propping up a falling rupee by selling dollars, which tightens liquidity. Since October, the RBI has spent $50bn from its forex reserves to shield the rupee.

Buyers must pay in rupees to purchase dollars, which reduces liquidity in the market. Maintaining a strong rupee through interventions reduces competitiveness by making Indian goods more expensive in global markets, leading to lower demand for exports.

"Why is the central bank shoring up the rupee? The policy is bad for the economy and exports. Possibly they are doing it because of optics. They don't want to show India's currency is weak," Mr Subramanian, a former economic adviser to the government, told the BBC.

Critics warn that the "hyping up the narrative" of India as the fastest-growing economy is hindering essential reforms to boost investment, exports and job creation. "We are still a poor country. Our per capita GDP is less than $3,000, while the US is at $86,000. If you say we are growing faster than them, it makes no sense at all," says Ms. Sengupta.

In other words, India requires a significantly higher and sustained growth rate to generate more jobs and raise incomes.

Boosting growth and consumption will not be easy in the short term. Lacking private investment, Himanshu suggests raising wages through government-run employment schemes to increase incomes and spur consumption. Others like Ms Sengupta advocate for reducing tariffs and attracting export investments moving away from China to countries like Vietnam.

The government remains upbeat over the India story: banks are strong, forex reserves are robust, finances stable and extreme poverty has declined. Chief economic adviser V Anantha Nageswaran says the latest GDP figure should not be over-interpreted. "We should not throw the baby out with the bathwater, as the underlying growth story remains intact," he said at a recent meeting.

Clearly the pace of growth could do with some picking up. That is why scepticism lingers. "There's no nation as ambitious for so long without taking [adequate] steps to fulfill that ambition," says Ms Sengupta. "Meanwhile, the headlines talk of India's age and decade - I'm waiting for that to materialise."

India: Is the world's fastest-growing big economy losing steam?

India's economy slumped to 5.4% , below the central bank's RBI's 7% forecast. What's going on?

www.bbc.com

www.bbc.com

These forecasts assume linear growth

China was suppose to overtake USA nominal gdp by 2028

Right now USA is 50% larger and china had not chance catching USA for 10/15,0 years now

India growth slowing down too from 7% to 5.5% so not convinced

China was suppose to overtake USA nominal gdp by 2028

Right now USA is 50% larger and china had not chance catching USA for 10/15,0 years now

India growth slowing down too from 7% to 5.5% so not convinced

onlinpunit

Trusted Member

How many times will you post this ? There are already 2 threads..Is the fastest-growing big economy losing steam?

10 hours ago

View attachment 87870

Between July and September, India's economy slumped to a seven-quarter low of 5.4%

Soutik Biswas

India correspondent•@soutik

BBC

Is the world's fastest-growing big economy losing steam?

The latest GDP numbers paint a sobering picture. Between July and September, India's economy slumped to a seven-quarter low of 5.4%, well below the Reserve Bank of India (RBI) forecast of 7%.

While it is still robust compared with developed nations, the figure signals a slowdown.

Economists attribute this to several factors. Consumer demand has weakened, private investment has been sluggish for years and government spending - an essential driver in recent years - has been pulled back. India's goods exports have long struggled, with their global share standing at a mere 2% in 2023.

Fast-moving consumer goods (FMCG) companies report tepid sales, while salary bills at publicly traded firms, a proxy for urban wages, shrank last quarter. Even the previously bullish RBI has revised its growth forecast to 6.6% for the financial year 2024-2025.

"All hell seems to have broken loose after the latest GDP numbers," says economist Rajeshwari Sengupta. "But this has been building up for a while. There's a clear slowdown and a serious demand problem."

Finance Minister Nirmala Sitharaman paints a brighter picture. She said last week that the decline was "not systemic" but a result of reducing government spending during an election-focused quarter. She expected third-quarter growth to offset the recent decline. India will probably remain the fastest-growing major economy despite challenges like stagnant wages affecting domestic consumption, slowing global demand and climate disruptions in agriculture, Sitharaman said.

View attachment 87867

India's inflation surged to 6.2% in October, mainly driven by high vegetable prices

Some – including a senior minister in the federal government, economists and a former member of RBI's monetary policy group – argue that the central bank's focus on curbing inflation has led to excessively restrictive interest rates, potentially stifling growth.

High rates make borrowing more expensive for businesses and consumers, and potentially reduce investments and dampen consumption, both key drivers of economic growth. The RBI has kept interest rates unchanged for nearly two years, primarily because of rising inflation.

India's inflation surged to 6.2% in October, breaching the central bank's target ceiling (4%) and reaching a 14-month high, according to official data. It was mainly driven by food prices, comprising half of the consumer price basket – vegetable prices, for example, rose to more than 40% in October. There are also growing signs that food price hikes are now influencing other everyday costs, or core inflation.

But high interest rates alone may not fully explain the slowing growth. "Lowering rates won't spur growth unless consumption demand is strong. Investors borrow and invest only when demand exists, and that's not the case now," says Himanshu, a development economist at Delhi's Jawaharlal Nehru University.

However, RBI's outgoing governor, Shaktikanta Das, believes India's "growth story remains intact", adding the "balance between inflation and growth is well poised".

Economists point out that despite record-high retail credit and rising unsecured loans - indicating people borrowing to finance consumption even amidst high rates - urban demand is weakening. Rural demand is a brighter spot, benefiting from a good monsoon and higher food prices.

View attachment 87868

India's central bank has kept interest rates unchanged for nearly two years, citing inflation risks

Ms Sengupta, an associate professor at Mumbai-based Indira Gandhi Institute of Development Research, told the BBC that the ongoing crisis was borne out by the fact that India's economy was operating on a "two-speed trajectory", driven by diverging performances in its "old economy and new economy".

The old economy comprising the vast informal sector, including medium and small scale industries, agriculture and traditional corporate sector, are still waiting for long-pending reforms.

In contrast, the new economy, defined by the boom in services exports post-Covid, experienced robust growth in 2022-23. Outsourcing 2.0 has been a key driver, with India emerging as the world's largest hub for global capability centres (GCCs), which do high-end offshore services work.

According to Deloitte, a consulting firm, over 50% of the world's GCCs are now based in India. These centres focus on R&D, engineering design and consulting services, generating $46bn (£36bn) in revenue and employing up to 2 million highly skilled workers.

"This influx of GCCs fuelled urban consumption by supporting demand for luxury goods, real estate and SUVs. For 2-2.5 years post-pandemic, this drove a surge in urban spending. With GCCs largely established and consumption patterns shifting, the urban spending lift is fading," says Ms Sengupta.

So the old economy appears to lack a growth catalyst while the new economy slows. Private investment is crucial, but without strong consumption demand, firms will not invest. Without investment to create jobs and boost incomes, consumption demand cannot recover. "It's a vicious cycle," says Ms Sengupta.

There are other confusing signals as well. India's average tariffs have risen from 5% in 2013-14 to 17% now, higher than Asian peers trading with the US. In a world of global value chains, where exporters rely on imports from multiple countries, high tariffs make goods more expensive for companies to trade, making it harder for them to compete in global markets.

View attachment 87869

Car sales have dropped by 14% in November - another signal of weakening demand

Then there is what economist Arvind Subramanian calls a "new twist in the tale".

Even as calls grow to lower interest rates and boost liquidity, the central bank is propping up a falling rupee by selling dollars, which tightens liquidity. Since October, the RBI has spent $50bn from its forex reserves to shield the rupee.

Buyers must pay in rupees to purchase dollars, which reduces liquidity in the market. Maintaining a strong rupee through interventions reduces competitiveness by making Indian goods more expensive in global markets, leading to lower demand for exports.

"Why is the central bank shoring up the rupee? The policy is bad for the economy and exports. Possibly they are doing it because of optics. They don't want to show India's currency is weak," Mr Subramanian, a former economic adviser to the government, told the BBC.

Critics warn that the "hyping up the narrative" of India as the fastest-growing economy is hindering essential reforms to boost investment, exports and job creation. "We are still a poor country. Our per capita GDP is less than $3,000, while the US is at $86,000. If you say we are growing faster than them, it makes no sense at all," says Ms. Sengupta.

In other words, India requires a significantly higher and sustained growth rate to generate more jobs and raise incomes.

Boosting growth and consumption will not be easy in the short term. Lacking private investment, Himanshu suggests raising wages through government-run employment schemes to increase incomes and spur consumption. Others like Ms Sengupta advocate for reducing tariffs and attracting export investments moving away from China to countries like Vietnam.

The government remains upbeat over the India story: banks are strong, forex reserves are robust, finances stable and extreme poverty has declined. Chief economic adviser V Anantha Nageswaran says the latest GDP figure should not be over-interpreted. "We should not throw the baby out with the bathwater, as the underlying growth story remains intact," he said at a recent meeting.

Clearly the pace of growth could do with some picking up. That is why scepticism lingers. "There's no nation as ambitious for so long without taking [adequate] steps to fulfill that ambition," says Ms Sengupta. "Meanwhile, the headlines talk of India's age and decade - I'm waiting for that to materialise."

India: Is the world's fastest-growing big economy losing steam?

India's economy slumped to 5.4% , below the central bank's RBI's 7% forecast. What's going on?

Indos

INT'L MOD

- Thread starter

- #8

China's Export Ban Sends Antimony Prices Soaring 40% in One Day

By Alex Kimani - Dec 04, 2024, 10:10 AM CSTAntimony prices soared 40% on Wednesday after China on Tuesday banned exports to the United States of several critical minerals. China enforced the existing limits on antimony, gallium, and germanium - critical minerals that have widespread military applications ahead of President-elect Donald Trump taking office next month.

"In principle, the export of gallium, germanium, antimony, and superhard materials to the United States shall not be permitted," Chinese Commerce Ministry said.

China is the world’s largest producer of antimony, accounting for 48% of global mined output. The country’s output in 2023 clocked in at 40,000 tonnes, nearly double Tajikistan’s 21,000 tonnes while Turkey was the third largest producer with 6,000 tonnes.

Antimony is considered a strategic metal used in military applications such as ammunition, infrared missiles and nuclear weapons as well as lead-acid storage batteries used in cars and brake pads thanks to its heat resistant properties. Antimony is also widely used in the solar sector to improve transparency for the cover glass on solar cells and is also used in the screens of smartphones.

“It’s a sign of the times. The military uses of Sb (antimony) are now the tail that wags the dog. Everyone needs it for armaments so it is better to hang onto it than sell it. This will put a real squeeze on the U.S. and European militaries,” Christopher Ecclestone, a principal and mining strategist at Hallgarten & Company in London, told CNN shortly after Beijing announced the curbs on antimony exports.

Not surprisingly, shares of rare metal producers are flying: shares of Hunan Gold Corporation, one of the biggest antimony producers, have returned 64% in the year-to-date while Perpetua Resources has rocketed 270% over the timeframe.

Beijing’s latest move comes the day after Washington's latest crackdown on China's chip sector, marking the escalation of an ongoing trade war between the world’s two largest economies. Last year, China announced that it would impose restrictions on exports of eight gallium and six germanium products starting August 2023 in retaliation for U.S. imposing trade restrictions and tariffs on Chinese-made products. On August 14, Beijing tightened the noose and announced export restrictions on antimony as part of the country's latest move to restrict critical mineral shipments.

By Alex Kimani for Oilprice.com

China's Export Ban Sends Antimony Prices Soaring 40% in One Day | OilPrice.com

China's export ban on critical minerals like antimony to the US sent prices soaring and threatens US military and tech industries.

oilprice.com

oilprice.com

Indos

INT'L MOD

- Thread starter

- #9

Articles

18 December 2024

We got another 25bp policy rate cut from the Fed, but updated projections and Chair Powell’s press conference confirms that the Fed is going to be much more cautious next year with sticky inflation and President Trump’s policy mix meaning a higher hurdle is required to justify rate cuts in 2025

Authors

James Knightley

Padhraic Garvey, CFA

Chris Turner

We got another 25bp rate cut, but in the press conference Chair Powell said they would be more cautious in 2025

The Federal Reserve has cut rates 25bp, as expected. This brings us to 100bp of cumulative cuts since September, but the Fed is indicating a much slower, more gradual series of rate cuts in the future. 50bp of cuts is now their baseline for 2025 based on the median of their individual forecast submissions, versus the 100bp that they were projecting in September.

The change of view is on the back of higher inflation forecasts predominantly – the core PCE deflator is now expected to end 2025 at 2.5% rather than 2.2% as previously thought and isn’t expected to get down to 2% until 2027. It also has to be viewed in the context whereby the economy is still growing robustly, the jobs market cooling, but not collapsing and equity markets at all-time highs.

50bp of policy rate cuts for 2025 was what the market was pricing ahead of time so reaction shouldn't have been that huge, but less confidence on inflation slowing sufficiently and the fact we had one FOMC member dissenting – Cleveland Fed President Hammack preferring no change – means markets aren’t fully pricing another cut until July with only 35bp now priced for 2025 in total. January’s FOMC is almost certainly going to see the Fed hold rates steady, but we will have a much clearer understanding of President-elect Trump's tariff, tax and spending intentions at the March FOMC meeting.

The Fed has previously suggested that they are not going to pre-empt those proposals and only take them into account when they are implemented. Nonetheless, given his policy thrust of immigration controls and tariffs, which could result in higher inflation, plus cuts to regulation and tax cuts designed to juice growth, we expected the Fed signals a shallower, slower path of easing through 2025. Ahead of time we were forecasting three 25bp rate cuts next year rather than the two 25bp the Fed suggest, but there is a huge amount of uncertainty given a lack of clarity on how far and how fast President Trump will go on policy, plus how quickly the jobs market is actually cooling and what this means for inflation. As such, we will keep our forecasts unchanged for now,

The 25bp cut itself was expected, but the big news is the larger-than-expected upward shift in the dot plot. The Fed now pitches the funds rate at 3.875% next year. That’s up 50bp from what they had before. In fairness though, the market’s discount had changed dramatically too in the past couple of months. Still, the market reaction is higher rates along the curve. Looking at the 2yr now at over 4.3%, it’s likely overreacted to the upside. While the 10yr rate is back to the 4.45%, back to where it was just post the Trump re-election. Little reason for this to collapse back lower based on what we know.

Noteworthy here is the upside shift in the market expectation for the effective fund rate for end-2025. This is now up to almost 4%. In other words the market is questioning whether the Fed delivers a final 25bp cut to get the funds rate below 4%. That pitches the implied “floor” for longer tenor rates at or about 4% (or just under). Contrast against that where the 10yr SOFR rate is now, at 3.95%. That’s essentially flat to the expected landing area for the funds rate. Something is mis-priced here. Either the Fed is going to cut by more than that. Or, and more likely, longer tenor rates are too low. As a call for 2025, we still see 4.5% for 10yr SOFR and 5%+ for the 10yr Treasury yields as viable targets.

The Fed also made an important technical adjustment to the overnight reverse repo rate (cut by 30bp), and now flat to the new Fed funds floor at 4.25% (cut by 25bp). This was broadly anticipated. It reduces the compensation obtainable at the reverse repo window, and should prompt less use of that window at the margin. Having a 5bp cushion made sense when the funds rate floor was a zero (to prevent a zero print). Now there is no cushion, but also no need for one. The effective funds rate should not be impacted in the sense that it should remain c.8bp above the floor. Although there can by a mild bias lower if anything.

Instead of quietly slipping into year-end, FX markets have been given a wake up call today that the Fed is looking at a higher inflation and interest rate profile over a multi-year horizon. Short-dated US swap rates have jumped 8bp on the news and pushed dollar rate differentials close to the widest levels of the year.

While a stronger dollar is very much a consensus (and our own view) for 2025, today’s bearish flattening of the US curve – telling us the Fed will not be providing as much monetary stimulus as first thought – is a clearly bullish factor for the dollar. It is also a bearish factor for the more pro-cyclical currencies in Europe and Asia and will weigh on commodity currencies – already under pressure on faltering Chinese growth and the prospect of Donald Trump’s trade agenda.

Expect EUR/USD to continue defying seasonal buying pressure – and we think 1.02/1.03 is possible over coming weeks. USD/JPY risks surging through 155 – although today’s hawkish Fed event makes it a little more likely that the Bank of Japan surprises with a rate hike tomorrow. And as above the commodity complex should stay under pressure. This is especially so for the Canadian dollar, which now has domestic turmoil to deal with as well.

Today’s event risk is going to prove a further headache for the People’s Bank of China as they try to hold onshore USD/CNY below 7.30 – even though USD/CNH can push well above that level. And bearish flattening of the US curve is bearish for most emerging currencies and especially the Brazilian real – which is off another 2% today. This heaps pressure on the Lula administration to deliver much needed fiscal consolidation – it cannot solely depend on the local central bank to save the real.

think.ing.com

think.ing.com

18 December 2024

Fed confirms a slower and shallower rate cut story for 2025

We got another 25bp policy rate cut from the Fed, but updated projections and Chair Powell’s press conference confirms that the Fed is going to be much more cautious next year with sticky inflation and President Trump’s policy mix meaning a higher hurdle is required to justify rate cuts in 2025

Authors

James Knightley

Padhraic Garvey, CFA

Chris Turner

We got another 25bp rate cut, but in the press conference Chair Powell said they would be more cautious in 2025

25bp from the Fed, but less in 2025

The Federal Reserve has cut rates 25bp, as expected. This brings us to 100bp of cumulative cuts since September, but the Fed is indicating a much slower, more gradual series of rate cuts in the future. 50bp of cuts is now their baseline for 2025 based on the median of their individual forecast submissions, versus the 100bp that they were projecting in September.

The change of view is on the back of higher inflation forecasts predominantly – the core PCE deflator is now expected to end 2025 at 2.5% rather than 2.2% as previously thought and isn’t expected to get down to 2% until 2027. It also has to be viewed in the context whereby the economy is still growing robustly, the jobs market cooling, but not collapsing and equity markets at all-time highs.

Federal Reserve forecasts versus September projections

Trump's plans for 2025 to determine how far the Fed can cut

50bp of policy rate cuts for 2025 was what the market was pricing ahead of time so reaction shouldn't have been that huge, but less confidence on inflation slowing sufficiently and the fact we had one FOMC member dissenting – Cleveland Fed President Hammack preferring no change – means markets aren’t fully pricing another cut until July with only 35bp now priced for 2025 in total. January’s FOMC is almost certainly going to see the Fed hold rates steady, but we will have a much clearer understanding of President-elect Trump's tariff, tax and spending intentions at the March FOMC meeting.

The Fed has previously suggested that they are not going to pre-empt those proposals and only take them into account when they are implemented. Nonetheless, given his policy thrust of immigration controls and tariffs, which could result in higher inflation, plus cuts to regulation and tax cuts designed to juice growth, we expected the Fed signals a shallower, slower path of easing through 2025. Ahead of time we were forecasting three 25bp rate cuts next year rather than the two 25bp the Fed suggest, but there is a huge amount of uncertainty given a lack of clarity on how far and how fast President Trump will go on policy, plus how quickly the jobs market is actually cooling and what this means for inflation. As such, we will keep our forecasts unchanged for now,

The recalibrated market discount for the funds rate exposes the 10yr rate as still too low here

The 25bp cut itself was expected, but the big news is the larger-than-expected upward shift in the dot plot. The Fed now pitches the funds rate at 3.875% next year. That’s up 50bp from what they had before. In fairness though, the market’s discount had changed dramatically too in the past couple of months. Still, the market reaction is higher rates along the curve. Looking at the 2yr now at over 4.3%, it’s likely overreacted to the upside. While the 10yr rate is back to the 4.45%, back to where it was just post the Trump re-election. Little reason for this to collapse back lower based on what we know.

Noteworthy here is the upside shift in the market expectation for the effective fund rate for end-2025. This is now up to almost 4%. In other words the market is questioning whether the Fed delivers a final 25bp cut to get the funds rate below 4%. That pitches the implied “floor” for longer tenor rates at or about 4% (or just under). Contrast against that where the 10yr SOFR rate is now, at 3.95%. That’s essentially flat to the expected landing area for the funds rate. Something is mis-priced here. Either the Fed is going to cut by more than that. Or, and more likely, longer tenor rates are too low. As a call for 2025, we still see 4.5% for 10yr SOFR and 5%+ for the 10yr Treasury yields as viable targets.

The Fed also made an important technical adjustment to the overnight reverse repo rate (cut by 30bp), and now flat to the new Fed funds floor at 4.25% (cut by 25bp). This was broadly anticipated. It reduces the compensation obtainable at the reverse repo window, and should prompt less use of that window at the margin. Having a 5bp cushion made sense when the funds rate floor was a zero (to prevent a zero print). Now there is no cushion, but also no need for one. The effective funds rate should not be impacted in the sense that it should remain c.8bp above the floor. Although there can by a mild bias lower if anything.

Fed fires up the next leg of the dollar rally

Instead of quietly slipping into year-end, FX markets have been given a wake up call today that the Fed is looking at a higher inflation and interest rate profile over a multi-year horizon. Short-dated US swap rates have jumped 8bp on the news and pushed dollar rate differentials close to the widest levels of the year.

While a stronger dollar is very much a consensus (and our own view) for 2025, today’s bearish flattening of the US curve – telling us the Fed will not be providing as much monetary stimulus as first thought – is a clearly bullish factor for the dollar. It is also a bearish factor for the more pro-cyclical currencies in Europe and Asia and will weigh on commodity currencies – already under pressure on faltering Chinese growth and the prospect of Donald Trump’s trade agenda.

Expect EUR/USD to continue defying seasonal buying pressure – and we think 1.02/1.03 is possible over coming weeks. USD/JPY risks surging through 155 – although today’s hawkish Fed event makes it a little more likely that the Bank of Japan surprises with a rate hike tomorrow. And as above the commodity complex should stay under pressure. This is especially so for the Canadian dollar, which now has domestic turmoil to deal with as well.

Today’s event risk is going to prove a further headache for the People’s Bank of China as they try to hold onshore USD/CNY below 7.30 – even though USD/CNH can push well above that level. And bearish flattening of the US curve is bearish for most emerging currencies and especially the Brazilian real – which is off another 2% today. This heaps pressure on the Lula administration to deliver much needed fiscal consolidation – it cannot solely depend on the local central bank to save the real.

Fed confirms a slower and shallower rate cut story for 2025

We got another 25bp policy rate cut from the Fed, but updated projections and Chair Powell’s press conference confirms that the Fed is going to be much more cautious next year

think.ing.com

ST1976

Trusted Member

here something we have Wikipedia as below

i find this GDP on PPP estimate still has to include 'undocumented' parts of GDP, the ratio of GDP we don't document.....

en.wikipedia.org

en.wikipedia.org

i find this GDP on PPP estimate still has to include 'undocumented' parts of GDP, the ratio of GDP we don't document.....

List of countries by GDP (PPP) - Wikipedia

Indos

INT'L MOD

- Thread starter

- #11

Currency concerns: on the rupee

The rupee’s rapid stumble poses a fresh challenge for the economy

Published - December 31, 2024 12:20 am ISTIt has been a tumultuous time for the Indian rupee even as the Reserve Bank of India (RBI) has been actively stepping into the foreign exchange market to stem its free fall in pursuit of what it calls an ‘orderly’ exchange movement.

The rupee had hit an all-time low of 85 to the U.S. dollar on December 19. Last Friday, it came precariously close to the 86-mark before a late intervention by the central bank pulled it back to 85.53. A confluence of factors at work have hurt the rupee in recent times, including the sustained outflows of foreign portfolio investments from securities markets after key indices peaked in late September.

Overstretched stock valuations, a demotivating corporate performance in the July-September quarter, and China’s economic stimulus, nudged emerging market portfolios from Mumbai to Beijing. The Donald Trump factor added a fresh headwind with the dollar strengthening since his U.S. presidential electoral victory, and emerging market currencies were further rattled by his warning of a 100% tariff on BRICS nations for a common currency plan to challenge the dominance of the U.S. dollar in global trade.

Even before fears about Mr. Trump’s generally protectionist stance on trade matters materialise, India’s goods trade story is sputtering. Record trade deficits and import bills are going to show up in this quarter’s current account deficit, which is expected to double from around 1.2% of GDP in the second quarter.

Services trade is still throwing up a surplus but the uncertainty around the H-1B visa regime will be a key monitorable, despite Mr. Trump’s latest soothing comments on the system. The previous RBI Governor, Shaktikanta Das, did well to forthrightly dismiss the BRICS currency as just an idea in the air, and stress that India has no de-dollarisation agenda.

The government must also issue an unequivocal statement to this effect in public fora and in diplomatic parleys to put the issue to rest. It is true that the currencies of other emerging markets have taken a bigger hit and a falling rupee bodes well for exporters, but India also needs to worry about importing inflation, especially on inelastic items such as edible oil and crude petroleum.

Moreover, foreign investment flows are uncertain as is the U.S. monetary policy outlook for 2025. There is also a limit to the extent the central bank can deploy forex reserves to manage the rupee’s trajectory, and the Finance Ministry has conceded that recent exchange rate movements cramp the freedom for monetary policymakers.

India’s present economic woes are linked to domestic drivers such as faltering consumption and reluctant investments. With the rupee coming under pressure, the country’s external resilience could be tested as well in 2025, and policymakers must gear up to manage this new risk.

Currency concerns: on the rupee

With the rupee coming under pressure, India’s external resilience could be tested as well in 2025

Indos

INT'L MOD

- Thread starter

- #12

Rupiah Might from US Dollar Ahead of New Year Night 2025

The rupiah closed to a 92 point against the US Dollar (USD), after previously strengthening 95 points at the level of 16,142 from the previous close at the level of 16,235.:strip_icc():format(webp)/kly-media-production/avatars/1913389/original/081531700_1585499592-photo_cms.jpg "Natasha Khairunisa Amani")

Natasha Khairunisa Amani

Updates 30 Dec 2024, 21:36 WIB

Liputan6.com, Jakarta Rupiah was observed to strengthen in the run-up to the New Year 2025 on Monday, December 30, 2024. The rupiah closed to a 92 point against the US Dollar (USD), having previously strengthened 95 points at the level of 16,142 from the previous close at the level of 16,235.

"As for tomorrow's trade, the Rupiah currency fluctative but closed strengthened in the range of 16,100 - 16,150," said Director of PT. Profit Forexindo Futures, Ibrahim Assuaibi in a statement in Jakarta, Monday (30/12/2024).

“The trading volume is low because of the shadowing New Year holidays and the day-data is a bit empty this week,” he said.

China Economic Data

China will release a PMI factory survey on Tuesday (31/12), while the U.S. ISM survey for December will be released on Friday.

Meanwhile, the consumer price index in Japan's capital Tokyo grew more than expected in December 2024 due to rising price pressures. This maintains an opportunity for short-term rate hikes by the Bank of Japan (BoJ).

Some of the Bank of Japan policymakers are looking at conditions that support a short-term rate hike, with one predicting action "in the near future," according to a summary of the opinion of the December meeting.

Beware of South Korea's Economy

The market is also still observing the development of South Korean presidential official, Prime Minister Han Duck-soo, who faces an impeachment vote, amid a political crisis triggered by the Constitutional Court's first hearing on the brief emergeticed martial law of President Yoon Suk Yeol's brief.The World Bank is raising its projections related to China's economic growth by 2024 and 2025.

However, the global financial body warned that household confidence and the levator, along with barriers in the property sector, will remain a hindrance next year.

Market Positive Response PPN Policy 12%

"The market responded positively about the enactment of VAT 12% which will take effect in January 2025 as a strategic step from the government but full of challenges," said Ibrahim.

As is known, this increase in VAT aims to strengthen the fiscal space to support the sustainability of long-term economic growth.

This policy is selective for the people and the economy. This step is also accompanied by the principle of justice, because basic goods, health services, education, and public transportation remain VAT-free, so that the burden of lower middle-income communities can be minimized.

Kemenkeu data shows, half of the incentives of VAT enjoyed by the community can afford. Examples of luxury goods groups that were previously freed VAT such as premium meat such as wagyu and kobe meat.

Likewise with premium services such as international schools and VIP health services. This is part of the government's consideration to raise VAT rather than income tax (PPh) to optimize state tax revenue.

The PPh tax base is smaller than VAT, because it is only imposed on certain taxpayers. Thus, the potential for state revenue from PPh is more limited than VAT that applies widely.

:strip_icc():format(jpeg)/kly-media-production/medias/4282588/original/045207500_1672910856-Imbas_potensi_perlambatan_ekonomi_nilai_rupiah_melemah_terhadap_dollar-ANGGA_7.jpg)

Rupiah Perkasa dari Dolar AS Jelang Malam Tahun Baru 2025

Rupiah ditutup menguat 92 point terhadap Dolar AS (USD), setelah sebelumnya sempat menguat 95 point di level 16.142 dari penutupan sebelumnya di level 16.235.

Indos

INT'L MOD

- Thread starter

- #13

The analysis is good, but you need to subscribe it in order to read the article

www.ft.com

www.ft.com

I will show you another article but with free content in below post

In charts: has the ‘India trade’ run out of steam?

Slowing growth and high inflation hit household incomes and raise questions about economic fundamentals

I will show you another article but with free content in below post

Indos

INT'L MOD

- Thread starter

- #14

Can India become the world’s third superpower? It faces huge challenges in 2025

If India is to realise its dreams of ranking alongside the US and China it must maintain high growth rates and ensure the benefits of development reach the population as a whole – no easy task, as Sheweta Sharma report

Wednesday 01 January 2025 19:07 GMT

In an exclusive interview with The Independent in September, Tony Blair made a bold claim – that India will rise to become a global superpower by 2050. “By the middle of this century, you’re going to have three superpowers – America, China, and you’re going to have India. All other countries are going to be small in comparison,” the former prime minister said.

India’s own prime minister, Narendra Modi, has set out similar aspirations, saying India will achieve “developed” status by 2047. He also vowed to make his country “the third largest economic superpower” by the end of his third term, though he made that pledge before a disappointing set of election results that saw him lose his outright majority in June 2024.

Most projections for India’s future strength are based on two simple facts – that it has now surpassed China to become the most populous country in the world, and its $3 trillion economy, already the fifth-largest, is growing at a faster rate than any other major nation.

Beyond simple economics, India’s importance has also risen geopolitically; courted by the US as a counterweight to China in the Asia-Pacific yet able to maintain strong ties to Russia at the same time, it has carved out a niche that could prove a model for other Global South nations. But does diplomatic independence equate to superpower status – or is it the ability to project power abroad that defines American and Chinese dominance?

India surpassed the UK as the world’s fifth-largest economy in 2023, and analysts at Morgan Stanley agree with Modi in predicting it will overtake Japan and Germany to reach third position by 2027.

Yet in a test to Modi’s ambitious plans, India’s economy is experiencing its slowest growth in the last two years, dampening the economic outlook for the full financial year. GDP grew at just 5.4 per cent in the July-September quarter, well below the Reserve Bank of India’s forecast of 7 per cent. Economists say there are signs that the expansion of the Indian economy is losing momentum.

Indian youths take a selfie on the newly built Signature Bridge in New Delhi in 2018 (AFP via Getty)

These high GDP growth figures also appear inconsistent with other economic indicators such as employment rates, private consumption and export performance. Consumer expenditure accounts for about 60 per cent of India’s GDP but has been badly affected by a slowdown in urban spending due to food inflation and sluggish real wage growth.

India’s goods exports, typically the main driver of a country’s economic growth, are also flatlining. In the 12 months leading up to August 2024, India’s total goods trade was valued at $1.1 trillion – the same level as it was two years ago.

And then there is the question of whether GDP growth really translates to improved outcomes for the population as a whole. It will be hard for India to claim superpower status for as long as it remains classified as a lower-middle-income country, a designation it has held since 2007, based on its per capita income of around $2,400 (£1,885). The World Bank estimates that it would take another 75 years for India’s average to reach even a quarter of the US.

In its 2024 report World Inequality Lab found that the current golden age of Indian billionaires has led to a dramatic surge in income inequality, placing India among the most unequal countries globally, surpassing the US, Brazil, and South Africa.

According to the economists behind the study, including renowned French economist Thomas Piketty, the income gap between India’s rich and poor has grown so vast that, by some metrics, income distribution in India was more equitable during British colonial rule than it is today.

Indian prime minister Narendra Modi, Russian president Vladimir Putin and Chinese president Xi Jinping at the Brics summit (AP)

Piketty, who was in Delhi for a conference in December, said India “should be active in taxing the rich” in order to distribute wealth better. But there are no signs that the eradication of economic inequality is a policy objective for Modi, who has been accused of maintaining close ties with the country’s billionaires and favouring the biggest business magnates with lucrative infrastructure projects, an allegation denied by the ruling BJP.

Former diplomat Shyam Saran, at a recent Chatham House discussion, argued that India undoubtedly has great potential based on its population, economic scale, and significant pool of scientific and technical talent.

“As far as India’s macro impact over the global landscape is concerned, it is certainly expanding, but in terms of the domestic metrics of development, I think those are changing very slowly. So, on the one hand, India is, in terms of GDP, today the fifth largest economy. But its ranking in the Human Development Index is abysmal, at 122 out of 191 countries, and progress has been very slow.” He says these contradictions have to be taken into account when looking at the possibility of India being the next superpower.

China’s economy, once a growth powerhouse, has struggled to regain its pre-pandemic momentum following three years of strict lockdowns. In the last quarter, China’s economy grew at 4.7 per cent, just below its government’s target of 5 per cent, reflecting broader challenges in sustaining its pre-pandemic pace.

Alicia Garcia-Herrero, chief economist for the Asia-Pacific at investment bank Natixis in Hong Kong, tells The Independent that India’s economy needs to grow around 6 per cent each year to become as large as China by 2050 while China’s growth rate will be decelerating up to 1 per cent from 2035 onwards.

“India will [then] be the size of China by 2050. But is this feasible?” she asks, highlighting the “slightly more worrisome” fall in Indian growth in the third quarter. “The forecast of 7 per cent growth for 2024 already seems quite impossible for India,” she adds.

Garcia-Herrero says it is now clear that India will outpace China in terms of growth for many years to come.

Women fill water from a municipal tank in Peth Taluka village, Nashik, Maharashtra (Getty)

“However, the challenges of becoming a superpower are significant. Technology and infrastructure are the main areas, but it’s broader than just that – it involves building a mature society with well-functioning institutions that are not overly influenced by the political party in power.”

Perhaps the clearest indicator of the inconsistency in India’s growth story is the deepening jobs crisis for educated young people, seen as one of the reasons many voters turned away from the BJP in the last election.

The share of educated youths among all unemployed people increased from 54.2 per cent in 2000 to 65.7 per cent in 2022 according to the latest figures by the International Labour Organization. It points to a situation where India, a country with an average age of just 29 years, is failing to utilise what is often described as its demographic dividend.

And there has been no significant rise in real wages in India since 2014, according to numbers computed by noted developmental economist Jean Dreze.

It’s not just the economy where India sees China as its closest competitor. Beijing has emerged as one of the major challenges for India under Modi, with security concerns outweighing economic considerations with its biggest trade partner.

Brutal hand-to-hand combat and high-altitude skirmishes between the armies of the two countries in their shared Himalayan border region since 2020 have led to deaths and injuries on both sides. The two nuclear powers have since mobilised tens of thousands of troops, backed by artillery, tanks, and fighter jets, along their de facto border.

A significant breakthrough came after almost three years of stalemate in October when Beijing and Delhi announced they had reached a deal to disengage from the friction points in the Himalayan border, suggesting a thaw in relations. Two days later, Modi and Xi Jinping were pictured shaking hands and exchanging smiles following their first bilateral meeting in five years. Yet the latest reports suggest there has still been no withdrawal of troops in the region by either side.

and Indian soldiers (background) clashing on the Line of Actual Control in the Galwan Valley")

A screengrab from 2021 shows Chinese (foreground) and Indian soldiers (background) clashing on the Line of Actual Control in the Galwan Valley (CCTV/AFP via Getty)

India’s refusal to back down in the years-long standoff reflects a general growth in confidence, one that has also seen New Delhi emboldened to tackle individuals who it sees as its enemies – even if they are based abroad. This approach was exemplified when defence minister Rajnath Singh, asked about extrajudicial killings in Pakistan that India had previously denied involvement in, finally declared: “We will go to Pakistan and kill” those who threaten India’s peace.

The Indian government is also accused of orchestrating targeted killings of those involved in a Sikh separatist movement abroad, in both the US and Canada. While the government has denied these allegations, it has vowed to defeat the pro-Khalistan movement internationally, having effectively quashed it at home.

“India has emerged more confident and more present under Modi’s leadership on the global stage, as Delhi has led itself with confidence and assertiveness that I think has really stood out and that has led to a number of favourable outcomes for India’s interests”, says Michael Kugelman, director of the Wilson Centre’s South Asia Institute.

“And that entails strengthened relations with the US as well as partnership with a number of regions and countries on unprecedented levels,” he adds.

In 2023, India became the chair of the G20 summit and hosted the biggest diplomatic event in the country in years. Modi presented India as the “Vishwaguru” or global teacher, and the government was accused of making a meal out of what was merely a rotating G20 presidency.

“India’s star shines a bit brighter on the global stage due to its relatively successful leadership of the G20. India’s ability to get leaders to agree on a statement that included a reference to Russia’s invasion of Ukraine, despite the issue being very divisive globally, was a notable achievement,” says Rick Rossow, director of US-India policy studies at the Centre for Strategic and International Studies (CSIS).

A slum area is covered up as part of a beautification project ahead of G20 (Getty)

“However, these achievements may not translate into tangible benefits like increased investment or development aid for India. The focus on global leadership under Modi’s tenure, while notable, is perceived by some as flashy rather than substantive.”

“So, at the end of the day, leadership in the G20 makes it feel like India is taking its role as a major power, but when you think about what other countries actually want from a major power, India still doesn’t have a lot of capacity to deliver, whether it’s aid, outbound investment, trade, that kind of thing.”

To solidify India’s status as a net security provider, Rossow says India needs to continue building out its power projection capabilities, accelerate the production of its second domestic carrier, and get more fourth-generation, maybe even fifth-generation fighter aircraft inducted into the air force and navy.

“I think there’s still a lot more that India can do and will do as the country continues to grow economically and in population,” says Rossow.

Can India become the world’s third superpower?

If India is to realise its dreams of ranking alongside the US and China it must maintain high growth rates and ensure the benefits of development reach the population as a whole – no easy task, as Shweta Sharma reports

Indos

INT'L MOD

- Thread starter

- #15

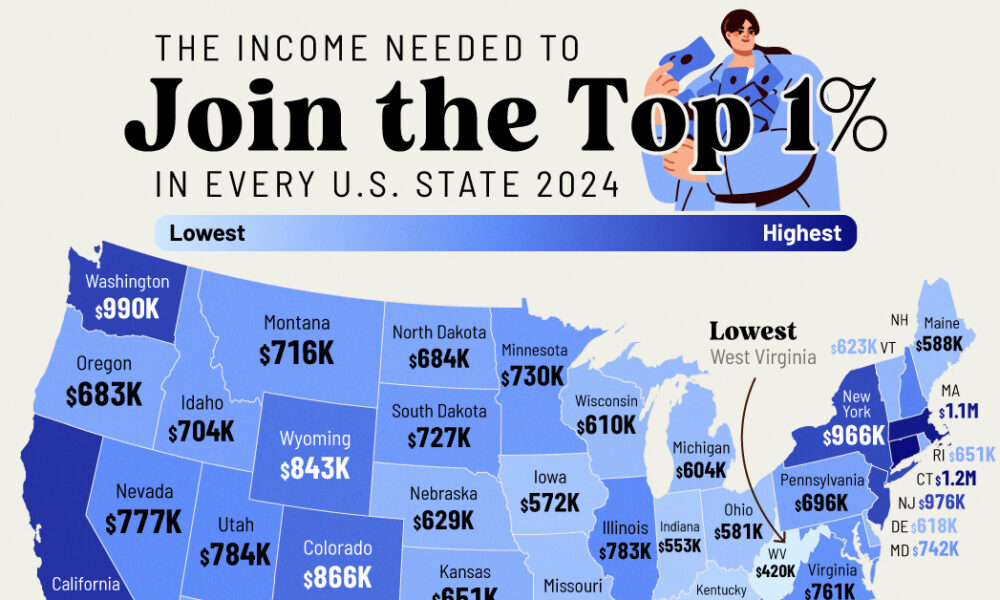

Mapped: The Income Needed to Join the Top 1% in Every U.S. State

Published on December 31, 2024

By Bruno Venditti

Graphics/Design:

Miranda Smith

Mapped: The Income Needed to Join the Top 1% in Every U.S. State

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

What does it take to join the top 1% of income earners in America?

Well, it depends on where you live. In some states, your annual income needs to crack $1 million to be among the state’s income elite—in others, it takes less than half of that to make the cut.

This graphic illustrates the income needed to be in the top 1% of earners in each state. The data was compiled by SmartAsset as of June 2024.

Methodology

SmartAsset analyzed 2021 IRS data for individual tax filers. Figures were adjusted to June 2024 dollars using the Bureau of Labor Statistics’ Consumer Price Index for All Urban Consumers (CPI-U), U.S. city average series for all items, not seasonally adjusted.

Key Takeaways

- Nationwide, it takes an income of $787,712 to be in the top 1% of earners.

- The median U.S. income is approximately $75,000, with half of Americans earning less.

- Earning over $1 million annually is required to join the top 1% in three states. Connecticut leads with the highest threshold at $1.2 million, followed by Massachusetts at $1.11 million, and California at $1.04 million. Meanwhile, in West Virginia, the threshold is almost a third of Connecticut’s at $420,000.

Mapped: The Income Needed to Join the Top 1% in Every U.S. State

It takes $787,000 to be in the top 1% of earners.

Users who are viewing this thread

Total: 1 (members: 0, guests: 1)

Pakistan Defence Latest

Country Watch Latest

-

-

-

-

TF-X / KAAN / Hürjet Turkish Fighter & Trainer Aircrafts News & Discussions (5 Viewers)

- Latest: Sinan

-