Navigation

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

More options

Style variation

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Chinese Economy: General News, Updates and Discussions

- Thread starter Beijingwalker

- Start date

More options

Who Replied?

Nan Yang

Registered Member

The Iran war’s unlikely winner: China’s shipyards

Mia Nurmamat

Published: 8:00am, 22 Apr 2026

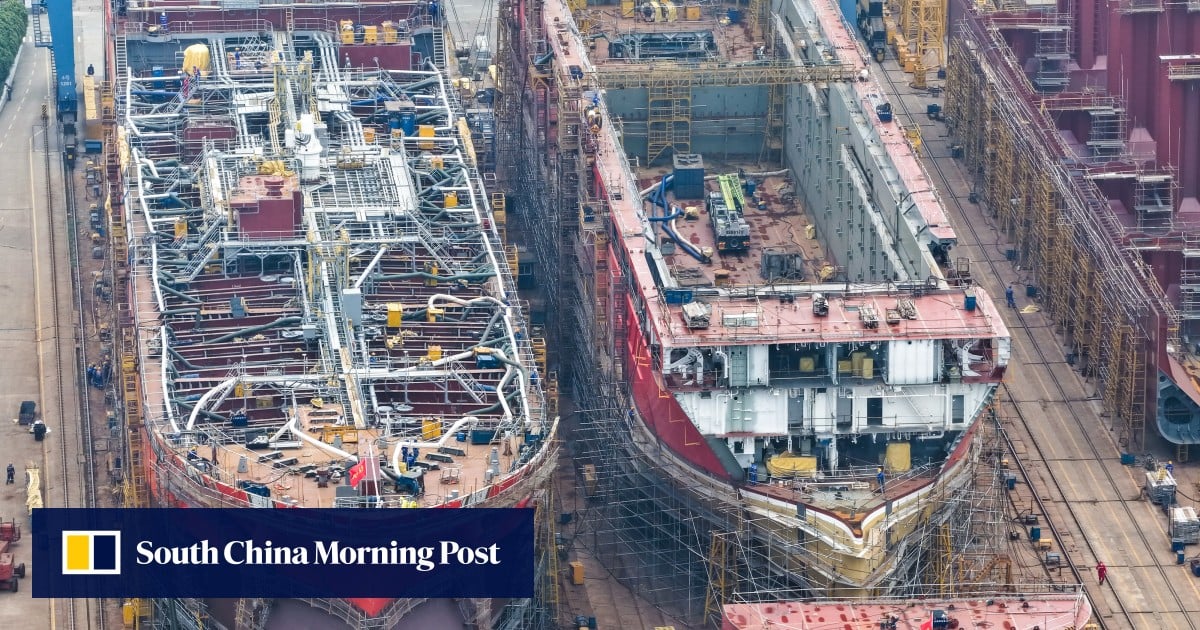

China’s shipyards are emerging as beneficiaries from the US-Israeli war on Iran, securing new orders as crude transport bottlenecks worsen and global demand for large oil tankers rises.

With the United States and Iran effectively blockading the Strait of Hormuz – a chokepoint that handles about a quarter of the world’s seaborne oil – shipping companies are racing to expand capacity, particularly in very large crude carriers (VLCCs) capable of transporting about 2 million barrels of oil per voyage.

The flurry of orders comes amid mounting pressure on global shipping. The strait has been largely blocked for eight weeks, sending crude oil prices to historic highs. Tankers are taking longer routes to avoid risky journeys through the Persian Gulf, exacerbating already tight fleets caused by ageing vessels and further straining supply.

But the disruption is opening new opportunities for Chinese shipbuilders, which are benefiting from strong capacity, lower costs and shorter delivery times. At least two Swiss firms and one Singapore-based company have placed VLCC orders with Chinese shipyards in recent weeks.

Switzerland’s Advantage Tankers, which had a long-standing reliance on South Korean shipyards, has placed an order in China for two 307,000-deadweight-tonne VLCCs. The vessels are scheduled for delivery in the second quarter of 2028 and the third quarter of 2029, respectively, the industry journal China Ship Survey reported last Thursday, though pricing was not disclosed.

Meanwhile, Geneva-based Mercuria Energy Group, one of the world’s leading independent commodity traders, has signed shipbuilding contracts in China worth nearly US$650 million. The order includes up to four VLCCs and two LR2 product tankers, with deliveries expected by 2029, according to the same journal, which is affiliated with the China Classification Society, a state-backed shipping body.

Source

www.scmp.com

www.scmp.com

China’s shipyards secure wave of oil tanker orders as Iran war drives demand

China already dominates global shipbuilding orders – and the Strait of Hormuz crisis appears to be boosting demand

Mia Nurmamat

Published: 8:00am, 22 Apr 2026

China’s shipyards are emerging as beneficiaries from the US-Israeli war on Iran, securing new orders as crude transport bottlenecks worsen and global demand for large oil tankers rises.

With the United States and Iran effectively blockading the Strait of Hormuz – a chokepoint that handles about a quarter of the world’s seaborne oil – shipping companies are racing to expand capacity, particularly in very large crude carriers (VLCCs) capable of transporting about 2 million barrels of oil per voyage.

The flurry of orders comes amid mounting pressure on global shipping. The strait has been largely blocked for eight weeks, sending crude oil prices to historic highs. Tankers are taking longer routes to avoid risky journeys through the Persian Gulf, exacerbating already tight fleets caused by ageing vessels and further straining supply.

But the disruption is opening new opportunities for Chinese shipbuilders, which are benefiting from strong capacity, lower costs and shorter delivery times. At least two Swiss firms and one Singapore-based company have placed VLCC orders with Chinese shipyards in recent weeks.

Switzerland’s Advantage Tankers, which had a long-standing reliance on South Korean shipyards, has placed an order in China for two 307,000-deadweight-tonne VLCCs. The vessels are scheduled for delivery in the second quarter of 2028 and the third quarter of 2029, respectively, the industry journal China Ship Survey reported last Thursday, though pricing was not disclosed.

Meanwhile, Geneva-based Mercuria Energy Group, one of the world’s leading independent commodity traders, has signed shipbuilding contracts in China worth nearly US$650 million. The order includes up to four VLCCs and two LR2 product tankers, with deliveries expected by 2029, according to the same journal, which is affiliated with the China Classification Society, a state-backed shipping body.

Source

The Iran war’s unlikely winner: China’s shipyards

China already dominates global shipbuilding orders – and the Strait of Hormuz crisis appears to be boosting demand.

Feroze

Trusted Member

I am Pro-China. I just post what is on BBC and Al Jazeera.Once again western propaganda

Fatman17

Moderator

Good for you.I am Pro-China. I just post what is on BBC and Al Jazeera.

Beijingwalker

VIP Member

- Thread starter

- #1,595

The Strait of Hormuz is today’s energy chokepoint. China is tomorrow’s.

As the global economy moves beyond oil, the strategic importance of the world’s most critical hydrocarbon chokepoint is likely to decline rapidly.

by FRANK JACOBSApril 22, 2026

, and major shipping routes and chokepoints, with oil reserves highlighted by pink circles of varying sizes.")

Data Sources: Port Economics, Management and Policy (PEMP), USGS, New York Times

KEY TAKEAWAYS

- Iran’s closure of the Strait of Hormuz highlights the world’s current dependence on Gulf oil — but that dependence is fading as decarbonization shifts demand to the critical minerals used in batteries and clean energy infrastructure.

- This shift will move the center of energy geopolitics from the Middle East to China, which not only has the world’s largest reserves of rare earth elements (REEs) but also most of the refining and processing capacity.

- A plus for America’s energy future: It sits on significant critical mineral deposits. A minus: It lacks the refining capacity to exploit them. That vulnerability could be the new chokepoint of the post-oil economy.

Why? Because we’ll be two decades further down the road to decarbonization. Oil will still flow out of the Strait, but it will matter significantly less to the world economy and the cost of driving in the U.S.

Electrification’s push and pull

As of early 2026, there are around 5.8 million EVs on U.S. roads, or just under 2% of all passenger vehicles. Projections for 2050 vary widely, from a low of 11% to a high of 75%.The chasm between those figures is due to two opposing forces pulling at the market. The case against accelerated electrification is bolstered by the recent slump in EV sales, which is driven, in part, by the dismantling of pro-EV measures, such as federal EV tax credits and EPA tailpipe emissions standards. But favoring accelerated electrification is the gas price spike due to the war in Iran, which has rekindled consumer interest in going electric.

Whether the number of EVs on the road grows quickly or slowly, it is safe to assume the vehicles will make up a significantly larger part of America’s car fleet 20 years from now than they do today — and that the people who drive them will be much better insulated against sudden oil price shocks.Decarbonization will help insulate the world economy against sudden oil price shocks like those caused by disruptions in the Strait of Hormuz.

The world economy as a whole should be better insulated, too, although predictions here also vary widely.

In November 2025, the International Energy Agency (IEA), which has been predicting for years that global oil demand would peak in 2030, introduced a Current Policies Scenario. It projects that, if current government policies remain in place (rather than changing as governments promise they will), global oil demand will continue to increase for the time being, postponing “peak oil” until mid-century.

It should be noted, however, that this change-nothing scenario was introduced following pressure from the Trump administration, which had been critical of the IEA’s pro-energy transition focus. The IEA’s Stated Policies Scenario still sees oil demand flattening around 2030 and then declining to 45% less than it is today by 2050. In the increasingly less achievable Net Zero Emissions by 2050 Scenario, oil and gas demand would drop by 75%.

More sustainable, yes — but also more stable?

All of those scenarios were written before the current war in Iran. The closure of the Strait of Hormuz (and the U.S. counterblockade) has added economic urgency to the energy transition that’s already underway worldwide. With petroleum getting more expensive and the price of energy from renewables dropping toward so-called grid parity, economic self-interest is replacing concern for the climate as the main driver of decarbonization.The Strait of Hormuz is currently the linchpin of the hydrocarbon-fueled economy. But as the world pivots toward more sustainable sources of energy, a new geopolitical order will emerge. Will it be any more safe and stable?

For Gulf locals, a new order may turn out to be a blessing in disguise, as the discovery of oil and gas has brought not just prosperity to the region, but also pollution, corruption, and conflict.Rare earth elements and other critical minerals are to the clean energy age what steel was to the Industrial Revolution.

The post-oil economy will have to be powered by something, though, so the Eye of Sauron will turn its gaze elsewhere — and because the infrastructure underpinning renewable energy relies on critical minerals and rare earth elements (REEs), places with access to them will fall within its sights.

What are critical minerals and REEs?

The terms critical minerals and REEs are frequently used interchangeably, but they are distinct and that distinction will become increasingly relevant.- Critical minerals constitute the broader category. According to the U.S. Geological Survey (USGS), these 60 materials are essential to America’s economy or national security and their supply chains are vulnerable to disruption. Critical minerals include lithium, cobalt, nickel, and graphite — key components of the lithium-ion batteries in smartphones, EVs, and the grid-scale storage systems that hold solar and wind power for later use.

- Rare earth elements (REEs) are a subset of critical minerals that includes 17 heavy metals: the 15 metallic chemical elements known as lanthanides (e.g., gadolinium, cerium, and samarium), plus scandium and yttrium. Despite their name, REEs are not so much “rare” as they are difficult to isolate. Cerium, for instance, is as common as copper, but it and the other REEs are typically found in compounds with other elements, making extraction difficult and costly. REEs are used in the infrastructure that surrounds batteries, the magnets found in EV motors and wind turbines, and other clean energy technologies.

Hydrocarbon reserves are concentrated largely in the Middle East, plus a handful of other countries, including Venezuela, Russia, Canada, and the U.S.

Critical minerals, including REEs, are spread out rather differently. Major potential sources include Russia, the U.S., Canada, Brazil, southern and eastern Africa, Australia, India, and Vietnam. But China holds nearly half of the global total of REE reserves: 44 out of roughly 92 million metric tons, according to the USGS.

If we follow the theory that resource-rich regions invariably attract superpower attention, then the parts of the world where these building blocks for the new energy paradigm can be found may have to start preparing for foreign bases in their backyards and foreign boots on their territory.

One country, Greenland, has already drawn some unwelcome attention from a superpower. In January, U.S. President Donald Trump explicitly admitted that “mineral rights” were one of the U.S.’s motivations for seeking control over the Danish territory.

China’s long game, carved in stone

Maps of hydrocarbon reserves and REE deposits have one thing in common: clear centers of gravity. For hydrocarbons, it’s the Middle East. For REEs, it’s China. But geological luck only partially explains China’s dominance in REEs and critical minerals.In 1992, during his famous Southern Tour of the country, Chinese leader Deng Xiaoping remarked that while “the Middle East has oil, China has rare earths.” That saying is now literally carved in stone in an industrial park in Inner Mongolia, which is home to one of China’s largest REE operations. It’s ahistorical to claim that Deng had an exact roadmap in mind for China’s rare-earth ascendancy, but his quote works as a retrospective prophecy. It’s also proof of China’s ability to play the long game — that’s the other reason it dominates in REEs, critical minerals, and the renewable energy sector as a whole.

It wasn’t always thus. Until the mid-1990s, the U.S. led global REE production. But then China swept in and used state subsidies, lower environmental standards, and a long-term industrial strategy to outcompete Western companies. By the 2010s, China had achieved near-total control of the global REE market. In 2015, Molycorp, the former flagship of American REE production, filed for bankruptcy.China now accounts for about 60% of global REE production — and Beijing is willing to go to great lengths to maintain its supply chain dominance.

China now accounts for about 60% of global REE production. Not content with its domestic deposits, the nation is acquiring REE and critical mineral projects around the world. In 2025, a Chinese company acquired an REE project in Tanzania at a nearly 200% premium over the market price — a sign of how far Beijing is willing to go to maintain its supply chain dominance.

But what makes its dominance so durable is not the mining of REEs, but the processing and refining of the minerals. China has about 90% of global REE processing capacity, a figure that rises to 99% for heavy rare earth elements, a subset of rarer and more valuable REEs.

That expertise is not easy to replicate. It’s taken Chinese companies decades to master the complex chemistry needed to separate and extract REEs from their compounds. That is why ore mined by Western companies often still ends up locked into Chinese processing agreements: There is effectively no viable, non-Chinese alternative.

The new energy chokepoints

While the map of global maritime chokepoints is fixed by geography, the importance of individual passages changes over time. The Strait of Hormuz, as mentioned, will almost certainly matter less in the future. The Suez Canal and the Bab el Mandeb Strait, on either side of the Red Sea, will likely stay vital as conduits for manufactured goods travelling from China to Europe, including EVs, solar panels, and other elements of the new energy order.China is also eyeing the use of polar shipping routes to reach Europe and North America, which would allow it to bypass traditional chokepoints. However, they’d introduce a new one: the Bering Strait — and that would give Russia and the U.S. leverage over Chinese trade.

But here is the crucial distinction between the ages of oil and critical minerals: Geography is no longer the primary factor in strategic power. With oil, control of strategic passages such as the Strait of Hormuz means control of the energy supply. With critical minerals, geography still matters, but the decisive factor is industrial.The infrastructure layer of the global clean energy transition is largely controlled by China, and its refineries are the chokepoints of the new global energy landscape.

Today, many countries can refine oil. But almost none can process REEs and other critical minerals at scale outside of China. This is the real endpoint of Deng’s 1992 vision: Chinese REE refineries are the chokepoints of the new global energy landscape.

And China has already demonstrated that it is not afraid to weaponize its dominance. In 2010, it banned REE exports to Japan over a fishing trawler incident. In 2023, it imposed a global ban on the export of REE separation and processing technologies — the ban was explicitly designed to prevent the development of refining capacity elsewhere.

For the renewables industry, this is a sobering reality: The infrastructure layer of the global clean energy transition is largely controlled by China — and will continue to be for the foreseeable future. To go green is, in effect, to go Chinese.

Rich in ore, poor in refineries

How does the global energy transition affect the U.S.? In terms of raw materials, the U.S. is, literally, resource-full. According to the USGS, the country is home to an estimated 3.6 million metric tons of REE reserves — a figure that likely understates the full picture.In 2024, the Mountain Pass facility in California produced an estimated 45,000 metric tons of REE mineral concentrates, making the U.S. the world’s second-largest producer. The recently opened Brook Mine in Wyoming — believed to sit on the largest unconventional REE deposit in the country, with an estimated value of $37 billion — adds further depth to the American resource picture. And more mines are in development.

But the uncomfortable reality is that mining is only the first step. For most of the past decade, the U.S. has been sending the ore it mines to China for processing. That creates strategic exposure: A single F-35 fighter jet contains over 900 pounds of REEs; a Virginia-class submarine contains around 9,200 pounds. REEs are also critical for technologies not directly related to clean energy, such as MRI and PET scanners. Should China choose to choke off REE exports, it would create crises in half a dozen vital industries, from defense to healthcare.The U.S. has the mines of the future, but not the refineries needed to close the production loop.

The U.S. is rightfully concerned. Since 2020, the Department of Defense (DOD) has allocated more than $439 million to domestic REE processing and magnet manufacturing projects. In 2025, it concluded a multibillion-dollar partnership to scale magnet production from 1,000 to 10,000 metric tons per year over the next decade. That would still be less than 10% of what China was producing in 2018, but it would be a step towards catching up.

Ultimately, Chinese dominance will be hard to displace in the near term. While the U.S. and Iran play tug-of-war with the Strait of Hormuz, Chinese megacorporations are fast replacing Middle Eastern petrostates as the kingmakers of the new global energy economy.

In that new world, the U.S. will have a seat at the table. The question is whether it will be a comfortable one. It has the mines of the future, but not the refineries needed to close the production loop. Unless and until that changes, the U.S. — and the rest of the world — will remain vulnerable to an energy chokehold that could make Hormuz look manageable in retrospect.

Beijingwalker

VIP Member

- Thread starter

- #1,596

China's new exports take on the world

For years, Made in China meant affordable, mass-produced goods. But a new generation of Chinese brands is emerging, often testing the water in Asia first before taking on global competitors.

China's new exports take on the world

A new generation of Chinese goods are riding a new wave as they become globally recognisable brands.

www.bbc.com

www.bbc.com

冖_冖

Registered Member

C-commerce tightens grip on Korea’s retail market

Chinese e-commerce platforms, or C-commerce, are tightening their grip on South Korea’s retail market, turning it into a cross-border price war playing to house

www.koreaherald.com

www.koreaherald.com

Chinese e-commerce tightens grip on Korea’s retail market

Published : April 22, 2026 - 14:34:31AliExpress, Temu gain ground in Korea as sellers tap cross-border channels

")

Chinese e-commerce platforms, or C-commerce, are tightening their grip on South Korea’s retail market, turning it into a cross-border price war playing to households feeling the pinch.

AliExpress and Temu sit at the forefront, with user bases that rank among the largest in Korea’s e-commerce market.

Data from WiseApp Retail shows that in the January-March period, AliExpress and Temu drew 8.57 million and 8 million monthly active users, respectively.

Barring Coupang, the two platforms have already overtaken most major domestic players, with 11street at 7.7 million users, Naver’s Plus Store at 7.52 million and Gmarket at 6.9 million. Combined, their 16.5 million users amount to half the reach of market leader Coupang, which logged 33.25 million.

Temu led all shopping apps in March with 749,320 new installs, according to IGAWorks’ Mobile Index. Naver Plus Store was the top domestic platform with 674,100 installs, while AliExpress added 369,020.

Their deepening foothold speaks to a recalibration in consumer behavior, industry officials said, as inflation eats into household budgets and pushes shoppers toward more practical, value-driven purchases over discretionary spending.

According to the Ministry of Data and Statistics, inflation-adjusted average monthly consumption spending fell 0.4 percent last year, marking the first annual decline in five years since 2020, even as nominal spending rose.

“As price becomes a central factor in consumer decisions, more users are gravitating toward low-cost Chinese e-commerce platforms,” one industry official said.

Others point to younger consumers, highly attuned to price and trends, as a key force behind the platforms’ rise.

That dynamic comes through most clearly in fashion, where Chinese online fashion platform Shein, for instance, saw users in their 20s and 30s nearly triple to 1.22 million in January from a year earlier, according to WiseApp Retail. The trend is already feeding through to trade data, with imports of Chinese clothing hitting a record $4.89 billion last year, up 8.1 percent on-year.

“With low brand loyalty and a readiness to adopt new platforms, consumers in their 10s and 20s can bring about rapid changes in the market as trends shift,” one industry source said. “If a platform fails to evolve alongside consumers, it will inevitably cede ground to the next generation of platforms.”

")

Global gateways for K-sellers

Though it may look like a unilateral broadside, Chinese platforms are also emerging as conduits connecting Korea’s e-commerce ecosystem to broader global markets.

JD.com’s recent tie-up with 11street, for example, allows Korean sellers to list products on its cross-border platform, JD Worldwide, with end-to-end fulfillment handled by JD Logistics. This enables them to focus on product competitiveness as more Korean fashion and beauty goods flow onto its platform.

“Through our Korean subsidiary, we intend to actively support the export of Korean brands to China via a direct sourcing model,” said Kim Min-hwa, head of JD.com Korea, at an export consultation session in March.

A similar playbook is unfolding at Gmarket, which has been leveraging Alibaba’s global platforms, such as Lazada, to expand cross-border sales. In March, Gmarket took part in a trade plaza in China, hosting export consultations for Korean firms. There, participants showed strong interest in its streamlined onboarding, integrated logistics and localized marketing capabilities.

Over the longer term, however, such partnerships could carry risks, some industry officials say.

Despite granting access to global logistics networks and overseas demand, they could foster dependence that erodes bargaining power over fees and data usage, as one industry official puts it.

“It seems imperative for Korean companies to leverage Chinese e-commerce platforms as a springboard, while retaining strategic control and building their own overseas networks,” the official noted.

")

冖_冖

Registered Member

BHP Shifts to Yuan-Based Pricing in Deal With China State Buyer - Caixin Global

BHP Shifts to Yuan-Based Pricing in Deal With China State Buyer - Landmark contract with state buyer CMRG challenges dollar benchmarks and boosts Beijing’s pricing ambitions

BHP Shifts to Yuan-Based Pricing in Deal With China State Buyer

By Luo GuopingPublished: Apr. 22, 2026 11:40 p.m. GMT+8

BHP Group has agreed to use a yuan-denominated spot index to price part of its iron ore sales to China’s state-backed centralized buyer, marking a shift that could reshape global commodity pricing.

The supply contract with China Mineral Resources Group (CMRG) advances Beijing’s push to strengthen its pricing power over key raw materials and challenges the dominance of U.S. dollar-based Western benchmarks.

Beijingwalker

VIP Member

- Thread starter

- #1,599

Public Medical service in Tibet before and after PRC

Beijingwalker

VIP Member

- Thread starter

- #1,600

China industrial profits surge at fastest pace since September in boost for economy

Eamonn SheridanApril 26 2026

- Chinese industrial profits accelerated to a seven-month high in March, with large firms posting a 15.8% year-on-year gain and first-quarter earnings rising 15.5%, reinforcing the resilience of China's manufacturing sector.

Summary

- China's industrial profits at large firms rose 15.8% year-on-year in March, fastest growth since September 2025

- January to March industrial profits rose 15.5% year-on-year, up from 15.2% in the prior reading

- Data covers industrial firms with annual revenue above 20 million yuan

- Strong profit growth driven by AI-related manufacturing demand, export momentum and improving pricing power

- Results come despite headwinds from the Iran war energy shock and global trade uncertainty

- China's industrial output rose 7.7% year-on-year in Q1 2026, underpinning the profit rebound

- Weak domestic consumption remains a structural drag but export demand and capital investment are filling the gap

The data, released by China's National Bureau of Statistics, showed that profits at industrial enterprises with annual revenue above 20 million yuan rose 15.8% in March from a year earlier, the fastest pace of growth since September last year. For the first quarter as a whole, profits were up 15.5% year-on-year, a modest acceleration from the prior reading of 15.2% and a result that will be seen as broadly encouraging given the scale of disruption caused by the Iran war and the associated energy shock.

The strength of China's industrial profit picture reflects several overlapping forces that have converged to support the manufacturing sector in recent months. Chief among them is the global artificial intelligence investment boom, which has driven surging demand for chips, advanced manufacturing equipment and the broader supply chain that feeds into AI infrastructure development. China has emerged as a central node in that supply chain, with first-quarter trade data showing imports of integrated circuits soaring 54% year-on-year in March alone, while exports of AI-related goods have continued to climb.

Export demand more broadly has provided a powerful tailwind. China's total exports rose 15% year-on-year in the first quarter of 2026, a result that has surprised economists to the upside and driven sharp upward revisions to full-year trade forecasts. Industrial firms have benefited directly from that external demand, with sectors including electric vehicles, solar panels, industrial machinery and electronics all reporting strong order books.

Pricing dynamics have also played a role in the profit rebound. After years of deflationary pressure that squeezed margins across the industrial sector, producer prices have begun to stabilise and in some categories recover, supported by higher global commodity prices and a pickup in domestic capital investment. That shift has allowed firms to rebuild profitability without relying solely on volume growth.

The results are particularly notable given the headwinds the sector has been navigating. The partial closure of the Strait of Hormuz following the outbreak of the Iran war has disrupted global energy flows and pushed up input costs for energy-intensive industries. Economists had warned that the shock could weigh meaningfully on Chinese industrial output and margins, but the first-quarter data suggests the impact has so far been more contained than feared. China's diversified energy supply base and strategic petroleum reserves have provided a degree of insulation, while the country's dominant position in green energy manufacturing has allowed it to benefit from the surge in global demand for alternatives to fossil fuels.

Domestic consumption remains the weak link in China's economic picture. Household spending has yet to mount a convincing recovery, leaving the industrial sector reliant on exports and fixed asset investment to sustain its momentum. Authorities have rolled out a series of incremental stimulus measures, but economists broadly agree that a more decisive shift in consumption patterns has yet to materialise. For now, however, the profit data suggests China's industrial engine is running at a pace that the broader economy can build on.

The acceleration in Chinese industrial profit growth is a positive signal for risk assets and commodity demand, suggesting the manufacturing sector is holding up better than many had feared despite the headwinds from the Iran war and global trade uncertainty. The 15.8% year-on-year March reading, the strongest since September last year, points to improving pricing power and volumes at large industrial firms, consistent with the strong trade data seen earlier in the month. The sequential improvement in the year-to-date figure from 15.2% to 15.5% adds further weight to the view that China's industrial economy is gaining momentum rather than losing it. For energy and metals markets, stronger Chinese industrial activity supports demand expectations. For equity markets, the data reduces near-term concerns about a sharp deterioration in corporate earnings driven by external shocks, though weak domestic consumption remains a structural risk to the sustainability of the recovery.

China industrial profits surge at fastest pace since September in boost for economy | investingLive

Chinese industrial profits accelerated to a seven-month high in March, with large firms posting a 15.8% year-on-year gain and first-quarter earnings rising 15.5%, reinforcing the resilience of China's manufacturing sector.

Beijingwalker

VIP Member

- Thread starter

- #1,601

China industrial profits jump 15.8% in March despite Iran war oil disruption

APR 26 20269:36 PM EDTKEY POINTS

- Industrial profits jumped 15.8% from a year earlier in March.

- In the first three months this year, enterprise profits expanded 15.5% from a year earlier.

- Large onshore inventories of Iranian oil and crude on tankers at sea have provided some cushion for the world’s biggest importer.

China industrial profits jump 15.8% in March despite Iran war oil disruption

Rising global oil prices have begun seeping into the domestic economy, squeezing margins for manufacturers dependent on imported raw materials.

Beijingwalker

VIP Member

- Thread starter

- #1,602

The Iran war has the world buying more clean energy. China stands to benefit the most

April 26 2026CNN Business

The war in Iran has sent oil-starved countries scrambling for fuel. Many are opting for energy alternatives — and turning to the renewables king of the planet: China.

Chinese exports of solar technology, batteries and electric vehicles all reached record highs in March, according to energy think tank Ember, a sign that the historic oil supply shock is accelerating the adoption of clean energy around the world.

After the US and Israel launched airstrikes against Iran in late February, the Iranian military effectively barricaded the Strait of Hormuz, cutting off about one-fifth of global oil and natural gas supply. Oil price volatility has surged as the conflict has expanded into the Middle East and negotiations to end the war have stalled.

Meanwhile, Asian nations that depend on the Middle East for energy imports are trying to mitigate fuel shortages by encouraging energy conservation and shortening work hours. As countries invest more in renewable energy, China stands to benefit as the world’s largest manufacturer of electric vehicles, wind turbines and solar panels.

A Thursday report from Ember said China exported 68 gigawatts of solar technology in March, surpassing the previous record set in August by 50%. Fifty countries set new records for Chinese solar imports, with the most significant growth coming from emerging markets in Asia and Africa hit hardest by the energy crisis, according to the think tank.

“Fossil shocks are boosting the solar surge,” said Euan Graham, senior analyst at Ember, in the report. “Solar has already become the engine of the global economy, and now the current fossil fuel price shocks are taking it up a gear.”

Ember said exports of solar, batteries and EVs in total rose 70% in March year over year, according to Chinese customs data. Those categories have become known in China as the “new three,” contributing significantly to the country’s GDP in place of clothing, home appliances and furniture exports that previously drove growth.

China’s battery exports reached $10 billion in March, with particularly high growth rates in the European Union, Australia and India, Ember said.

Paradigm shifts

Uncertainty over when the Strait of Hormuz will reopen has spurred deeper regional anxieties about energy security, helping to hasten the transition to clean energy, analysts said.The US and Iran have agreed to a ceasefire while they negotiate terms to end the war, but tensions in the strait have remained elevated. Both US and Iranian forces have seized ships in the critical passageway, subduing further attempts to transit through.

The oil crisis has also reshuffled regional trade and relationships as nations seek to insulate themselves from the supply shock. Building out renewable capacity has been one way to cushion the blow.

“As we face the second fossil fuel shock in less than 5 years, the lesson for our country is clear: The era of fossil fuel security is over, and the era of clean energy security must come of age,” said UK Energy Secretary Ed Miliband, in a statement this week on the need to reduce the nation’s reliance on gas for electricity.

In China, massive state investment in green energy industries has bolstered its energy self-sufficiency, reducing its exposure to the oil shortage. Its dominance in renewable technology has also granted the country more geopolitical and economic influence as it exports its technology.

Pakistan has been spared some of the impact from the war, since it began drastically importing cheap Chinese solar panels a few years ago. Using solar energy rather than costly oil imports is estimated to save the country billions of dollars each year.

A robotic arm works on photovoltaic modules at the workshop of Alternative Energy Solar Co., Ltd. on December 17, 2025, in Huaian, Jiangsu Province of China.

VCG/Visual China Group/VCG via Getty Images

“China has been regarded as a low-cost supplier, but is increasingly treated as a long-term partner in the energy transition,” wrote Jeong Won Kim, a senior research fellow at the Energy Studies Institute at the National University of Singapore.

And it’s not just solar panels. Ember analysts estimated that global EV adoption had reduced oil consumption by about 1.7 million barrels last year — and as oil prices rose at the start of the Middle East conflict, Chinese state media reported that the country’s EV giants had seen an overseas sales surge.

According to the China Passenger Car Association, Chinese exports of electric vehicles and hybrids hit a record high in March, increasing 140% compared with the same period a year ago.

Analysts said part of the surge in solar sales last month was due to stockpiling before China discontinued a tax rebate in April. Lauri Myllyvirta, co-founder of the Centre for Research on Energy and Clean Air, said it’s unlikely the significant increase in exports from March will be sustainable.

Still, the conflict in the Middle East has strengthened the long-term case for alternative energy, he added.

“The fall in the costs of solar power and batteries, and now the higher and more volatile fossil fuel prices have made solar a no-brainer for a large share of global electricity consumers,” he said.

Beijingwalker

VIP Member

- Thread starter

- #1,603

The Chinese sports brand taking on Nike and Adidas

BBCOsmond Chia

April 26 2026

Chinese sportswear brand Anta counts Olympic freestyle skier Eileen Gu among its brand ambassadors

China's economy was just starting to open up in the late 1980s when a determined high school dropout made his way to Beijing with 600 pairs of shoes.

Ding Shizhong had them made in a relative's factory and now he was going to sell them. The money he earned paid for his first workshop where he began making footwear for other companies.

The 17-year-old was one of China's many newly minted entrepreneurs as capitalism took off under the watchful eye of its Communist Party rulers.

But, as it turns out, Ding had much bigger plans.

His business has since grown into a sportswear powerhouse called Anta, which has been building a stable of international brands, including Arc'teryx and Salomon. Most recently it bought a stake in Puma.

Now it is trying to take on the likes of Nike and Adidas, a goal that Ding spelled out in 2005: "We don't want to be the Nike of China, but the Anta of the world."

Anta may not be a household name in the West yet, but it has more than 10,000 shops in China and sponsors top athletes like freestyle skier Eileen Gu.

In February, it opened its first US outlet - a flagship store in Los Angeles' upscale Beverly Hills area.

The company's global push, which comes as Donald Trump aims to bring factory jobs back to the US with tariffs, highlights just how essential and competitive Chinese supply chains have become for manufacturing.

The rise of Anta - which means "safe steps" - is not exactly unique. Decades of being the world's factory have given several ambitious Chinese companies the opportunity to take on the very firms they once counted as customers.

From shoe maker to global brand

Founded in 1991, Anta began far from the glitz and the glamour of Beverly Hills as a small manufacturer in Jinjiang city in the south-eastern province of Fujian.Jinjiang grew rapidly from a quiet agricultural county into the "shoe capital" of the world as part of the government's plan to create specific industries in different provinces.

Soon, there was an influx of investment from sneaker giants who were in search of overseas factories that could help bring down their production costs.

Several clusters focusing on different sorts of footwear emerged in Jinjiang and neighbouring cities along the eastern coast, each with its own specialised supply chain.

At the Jinjiang hub's core lies Chendai town, an area of around 40 sq km (15.4 sq miles) that is home to thousands of factories and suppliers. The district helped cement the city's reputation making shoes for global brands such as Nike and Adidas.

Each hub brought together suppliers of laces, soles and fabric, as well as logistics firms that help to quickly turn designs into store-ready products and ship them out.

By 2005, Fujian alone accounted for nearly a fifth of the world's shoes, according to estimates by the UN.

As much as a third of Jinjiang's workers are still employed by one of thousands of shoe-makers in the city, which is among the highest-earning economic districts in China.

Something similar has played out in various parts of China - Jinjiang was just one of many manufacturing clusters on the eastern coast alone. The others made clothes or electronics.

This level of specialisation in manufacturing was unseen elsewhere in the world at the time, says University of Bath associate professor Fei Qin, who studied factories across eastern China in the 2000s.

As foreign customers flocked to strike deals with these factories, the country reaped more than income.

"They learned not only how to make more, but how to produce better, faster and more consistently," Fei adds.

It was along these streets that Anta grew, making shoes in bulk and cheaply for global brands.

It established a vast distribution network to retailers across China, which is crucial for manufacturers seeking to expand.

At the same time, Anta was slowly getting its name out domestically, opening new shops and partnering with major sporting events, including national basketball and table tennis competitions.

Firms like Anta know that there is more value in being a known brand rather than a subcontractor, Fei says.

In 2007, Anta listed on the Hong Kong Stock Exchange, raising around HKD3.5bn (£330m; $450m) - a record then for a Chinese sports company.

Branding consultant Wei Kan, who worked with Converse and Nike in China, says Anta had stood out to him because of its fully-fledged production hub that allowed it to design and sell shoes faster than its rivals.

It was also among the few Chinese firms that targeted the same buyers as big Western brands, Kan says.

Companies like Anta, which start off making goods for global brands, gradually learn the fundamentals of managing the business, do well in China and "naturally go on to bigger things", Kan adds.

There are many others such as technology firm Xiaomi, which began as a software developer customising Android-based systems, before making its own phones, electronics and now, electric vehicles (EVs).

Likewise, DJI made gear for cameras and drone components before it became an international drone maker in its own right.

The best-known example is perhaps BYD, once a battery-maker for EV pioneers like Tesla and now the world's top manufacturer for the sector.

"Each of these firms are now giants in their fields," Kan says.

Wooing the West

Anta is now eyeing markets in the West.It runs more than 12,000 shops in China. The company also has more than 460 outlets outside of the country, with plans to have 1,000 shops operating in South East Asia alone in the next three years.

But Nike which still has the biggest market share in sports footwear only has 1,000 shops across the world.

Chinese firms have been known to expand quickly within the country, before venturing abroad where they encounter more challenges while scaling up.

For one there is a perception challenge. Chinese products are often viewed as cheap, low-quality or copycat goods.

Anta has tried to beat that with acquisitions, as part of an approach it calls a "multi-brand strategy". The first big move was buying the rights to Fila in China in 2009 and turning the Italy-founded brand into a major earner for its business, says Elisa Harca from Chinese marketing agency Red Ant Asia.

In 2019, Anta bought a controlling stake in Finnish athletics brand Amer Sports. The deal gave Anta control of Amer's companies, which included upmarket brands Arc'teryx and Salomon.

Anta also owns Wilson, the US maker of tennis rackets and balls used by the National Basketball Association. And this year, it bought a 29% stake in Puma, pledging to help the German firm grow in China.

Kyrie Irving with the NBA ball by Wilson - now one of Anta's brands

These are moves that help Anta avoid "forcing" its goods into every market and instead use its Western brands as a gateway, says business analyst Rufio Zhu from global sports marketing agency IMG.

That way Anta can reach buyers who may be wary of a "made in China" brand, Zhu says.

Celebrity sponsorships are a key commodity for a truly global brand. Nike, for instance, had its groundbreaking deal with Michael Jordan in the 1980s.

Anta has signed basketball players like Klay Thompson and Kyrie Irving but deals of the kind that earned Nike or Adidas their brand are yet to happen.

And being a Chinese brand comes with hurdles given Beijing's rocky relationship with the West and especially the US.

American-born skier Eileen Gu - an Anta brand ambassador - proved a polarising figure after her choice to represent China over the US at the OIympics came under scrutiny.

Companies that grow big need to toe the line between China and the West, Kan says. "Brands like Anta need to be ready for it."

Anta has more than 10,000 shops in China

A turning tide

Anta's rise comes as rivals like Nike and Adidas face their own challenges globally and in China.US tariffs have hit their earnings given they import goods made in Asia. Nike is also fighting to revive sales since its e‑commerce push backfired after Covid-19, and demand in China has slowed as well because of low consumption.

Their struggles put Anta in a favourable position abroad, especially given consumers' growing appetite for other brands, says sports marketer Zhu.

"The question isn't whether Anta will raise their profile. It's whether competitors can adapt quickly enough to defend their home turf."

Meanwhile, China is "setting its manufacturers up for the future" by rapidly deploying robots in factories, speeding up production and potentially cutting costs, Fei adds.

The opening of Anta's first US outlet came after years of selling in the country through department stores.

Its walls are lined with shelves of sneakers and basketball shoes - markets that Anta needs to win in the US to compete with Nike or Adidas.

The company admits that it has some way to go.

"We're realistic about the competition but the global sportswear landscape is not a zero-sum game," an Anta spokesperson tells the BBC.

"We are confident that sports lovers will recognise Anta's innovations and brand value."

Anta: The Chinese sports brand taking on Nike and Adidas

Now one of the biggest sportswear firms, Anta's rise follows a playbook adopted by many Chinese giants.

www.bbc.com

Beijingwalker

VIP Member

- Thread starter

- #1,604

Taiwan's stock market surpasses the UK's despite having less than a quarter of the UK's economy — AI boom propels Taiwan forward, TSMC alone accounts for more than 40% of Taiwan's total market value

NewsBy Luke James published 15 hours ago

Taiwan's stock market is now valued at $4.3 trillion, driven by AI.

(Image credit: Getty Images)

Taiwan's stock market is now worth more than the United Kingdom's, according to recent Bloomberg data, in a shift driven almost entirely by the insatiable global appetite for AI chips. The island's listed companies carry a combined valuation of roughly $4.3 trillion, edging past Europe's largest equity market, despite Taiwan's economy being less than a quarter the size of the UK's. South Korea, powered by Samsung and SK hynix, is roughly $140 billion behind and closing fast.

As for Taiwan’s stock market constituents, TSMC makes up the bulk, with a market cap of approximately US$1.98 trillion, or 40% of Taiwan’s entire stock market value. No other major economy has this degree of single-company dependence. By comparison, Apple represents roughly 7% of the S&P 500.

On Thursday, Taiwan's Financial Supervisory Commission raised the single-stock investment cap for local equity funds from 10% to 25% of a fund's net asset value. The change applies only to companies whose market weighting exceeds 10%, a threshold TSMC alone meets. That adjustment triggered a 4.3% jump in TSMC shares on Friday and pushed the benchmark TAIEX up 2.7%, according to Taiwanese media.

TSMC reported record first-quarter earnings last week, with net income up 40.6% year-over-year to roughly $18 billion. The company raised its full-year revenue guidance to more than 30% growth and confirmed plans to add another 3nm fab to meet AI demand, which it expects to outstrip supply through 2027.

South Korea's market, KOSPI, has already overtaken both Germany and France this year and is up 44% in 2026. Samsung and SK hynix account for nearly half the index's total weighting. The former’s share price has nearly quadrupled since the start of 2025, while SK hynix has risen roughly sixfold over the same period. These gains reflect the ongoing memory supercycle, with demand for HBM far exceeding current production capacity.

William Bratton, head of cash equity research for Asia-Pacific at BNP Paribas, told the Financial Times that, aside from ASML, European-listed equities have almost no exposure to the current AI hardware buildout. He added that South Korea could overtake the UK as well if the current rally continues.

The disparity between these semiconductor-heavy Asian markets and Europe highlights how narrowly the financial benefits of the AI infrastructure boom are distributed. Taiwan's GDP is roughly $977 billion, according to IMF estimates, versus the UK's $4.3 trillion. While the gap between those two economies hasn’t changed, the gap between their stock markets has.

Taiwan's stock market surpasses the UK's despite having less than a quarter of the UK's economy — AI boom propels Taiwan forward, TSMC alone accounts for more than 40% of Taiwan's total market value

Taiwan's stock market is now valued at $4.3 trillion, driven by AI.

Beijingwalker

VIP Member

- Thread starter

- #1,605

Hong Kong leads global IPO fundraising this year, surpassing HK$140b: official

By Zhang YiyiPublished: Apr 26, 2026 09:52 PM

View of Hong Kong Exchanges and Clearing Ltd Photo: VCG

Hong Kong Financial Secretary Paul Chan Mo-po said on Sunday that the city has remained the world's top IPO market this year, with fundraising exceeding HK$140 billion ($17.87 billion) as of last week and average daily turnover topping HK$280 billion since March, highlighting the resilience of its financial markets amid global uncertainties.

In his blog, Chan wrote that last week saw the city's largest IPO listing of the year, and Hong Kong remains first globally in new share fundraising this year. These developments demonstrate that despite global uncertainties, the city's financial market remains unstoppable thanks to the joint efforts of the government and the industry, he wrote.

Chan said that Hong Kong's role and capabilities as an international financial center are continually being strengthened and enhanced. Even amid the challenges posed by a shifting geopolitical landscape, the city continues to pursue innovation and expand partnerships to unlock new growth opportunities.

He said that Hong Kong is actively developing its international gold trading market. Last week, the city's largest gold ETF was launched, supporting physical gold subscription and redemption, allowing trading and storage to take place locally, which helps Hong Kong gradually build a complete gold industry and value chain.

Chan added that Hong Kong has signed mutual recognition agreements with 20 exchanges worldwide to facilitate dual listings and create a broader network of market collaboration. The city is also actively exploring including the Malaysia Exchange on the "recognized stock exchange" list to attract new capital and listings.

The flurry of launches, despite a darkening global economic picture due to the war in the Middle East, builds on a buoyant start to 2026 for Hong Kong's listings market, which has recorded its strongest start to any year since 2021, Reuters reported.

Hong Kong's IPO market saw issuers raising about $11.64 billion in the first quarter of 2026, up 385 percent year-on-year, according to LSEG data as of March 18, Reuters reported. Fueled by IPOs from the Chinese mainland, Hong Kong ranked as the world's top listing venue in 2025, with total equity capital market fundraising jumping 164 percent to $103 billion, according to exchange data, it said.

Bian Yongzu, executive deputy editor-in-chief of Modernization of Management magazine, told the Global Times on Sunday that Hong Kong's continued lead in global IPO fundraising is underpinned by its strong institutional foundations.

Bian said that Hong Kong's highly open financial system is a key advantage. With free capital flows and transparent regulation, global capital can be allocated efficiently, making the city an attractive venue for listings and fundraising.

Also, backed by the vast economic hinterland of the Chinese mainland, a steady pipeline of fast-growing companies continues to generate strong financing demand, providing a stable source of listings for the market, according to the expert.

Chan wrote that financial markets are steadily improving, while a rebound in residential property and other asset markets has boosted consumer confidence. The latest data shows the first-quarter unemployment rate fell to 3.7 percent, with the retail and dining sectors trending upward.

Chan added that with the upcoming May Day holidays, Hong Kong's immigration department expects about 980,000 Chinese mainland visitors, up about 7 percent from last year, which will boost the retail, dining, and hotel sectors. The Hong Kong Special Administrative Region government will ensure supporting services are in place to provide a better experience for travelers.

By Zhang YiyiPublished: Apr 26, 2026 09:52 PM

View of Hong Kong Exchanges and Clearing Ltd Photo: VCG

Hong Kong Financial Secretary Paul Chan Mo-po said on Sunday that the city has remained the world's top IPO market this year, with fundraising exceeding HK$140 billion ($17.87 billion) as of last week and average daily turnover topping HK$280 billion since March, highlighting the resilience of its financial markets amid global uncertainties.

In his blog, Chan wrote that last week saw the city's largest IPO listing of the year, and Hong Kong remains first globally in new share fundraising this year. These developments demonstrate that despite global uncertainties, the city's financial market remains unstoppable thanks to the joint efforts of the government and the industry, he wrote.

Chan said that Hong Kong's role and capabilities as an international financial center are continually being strengthened and enhanced. Even amid the challenges posed by a shifting geopolitical landscape, the city continues to pursue innovation and expand partnerships to unlock new growth opportunities.

He said that Hong Kong is actively developing its international gold trading market. Last week, the city's largest gold ETF was launched, supporting physical gold subscription and redemption, allowing trading and storage to take place locally, which helps Hong Kong gradually build a complete gold industry and value chain.

Chan added that Hong Kong has signed mutual recognition agreements with 20 exchanges worldwide to facilitate dual listings and create a broader network of market collaboration. The city is also actively exploring including the Malaysia Exchange on the "recognized stock exchange" list to attract new capital and listings.

The flurry of launches, despite a darkening global economic picture due to the war in the Middle East, builds on a buoyant start to 2026 for Hong Kong's listings market, which has recorded its strongest start to any year since 2021, Reuters reported.

Hong Kong's IPO market saw issuers raising about $11.64 billion in the first quarter of 2026, up 385 percent year-on-year, according to LSEG data as of March 18, Reuters reported. Fueled by IPOs from the Chinese mainland, Hong Kong ranked as the world's top listing venue in 2025, with total equity capital market fundraising jumping 164 percent to $103 billion, according to exchange data, it said.

Bian Yongzu, executive deputy editor-in-chief of Modernization of Management magazine, told the Global Times on Sunday that Hong Kong's continued lead in global IPO fundraising is underpinned by its strong institutional foundations.

Bian said that Hong Kong's highly open financial system is a key advantage. With free capital flows and transparent regulation, global capital can be allocated efficiently, making the city an attractive venue for listings and fundraising.

Also, backed by the vast economic hinterland of the Chinese mainland, a steady pipeline of fast-growing companies continues to generate strong financing demand, providing a stable source of listings for the market, according to the expert.

Chan wrote that financial markets are steadily improving, while a rebound in residential property and other asset markets has boosted consumer confidence. The latest data shows the first-quarter unemployment rate fell to 3.7 percent, with the retail and dining sectors trending upward.

Chan added that with the upcoming May Day holidays, Hong Kong's immigration department expects about 980,000 Chinese mainland visitors, up about 7 percent from last year, which will boost the retail, dining, and hotel sectors. The Hong Kong Special Administrative Region government will ensure supporting services are in place to provide a better experience for travelers.

Users who are viewing this thread

Total: 6 (members: 0, guests: 6)

Pakistan Defence Latest

Country Watch Latest

-

-

The deal for 48 F-35 fighters.. How can it reshape Saudi air power in the Middle East? (9 Viewers)

The deal for 48 F-35 fighters.. How can it reshape Saudi air power in the Middle East? (9 Viewers)- Latest: KAL-EL

-

-

-

Latest Posts

-

-

-

Makkah Joint Defense Agreement: Turkey, Saudi Arabia, and Pakistan, news & updates (49 Viewers)

- Latest: hyperman

-

Another top router maker accused of firmware having backdoors — Chinese giant Zbtlink halts downloads to fix issue (11 Viewers)

- Latest: Hamartia Antidote

-