ST1976

Trusted Member

India GDP per capita is similar to that of Pakistan or Bangladeshi. Not to that of China. India should be between an under developed country or a developing country. Also, Thailand and Vietnam are mistaken categorized as developing. There is no way India should be a newly developed country as India is behind Vietnam or Thailand.

Just noticed Russia is ranked as less than India at development. No Russians poop openly. Horrible ranking and totally untrustworthy. It’s either a CIA ranking or Indian ranking.

Newly Industrialized Country (NIC) Definition

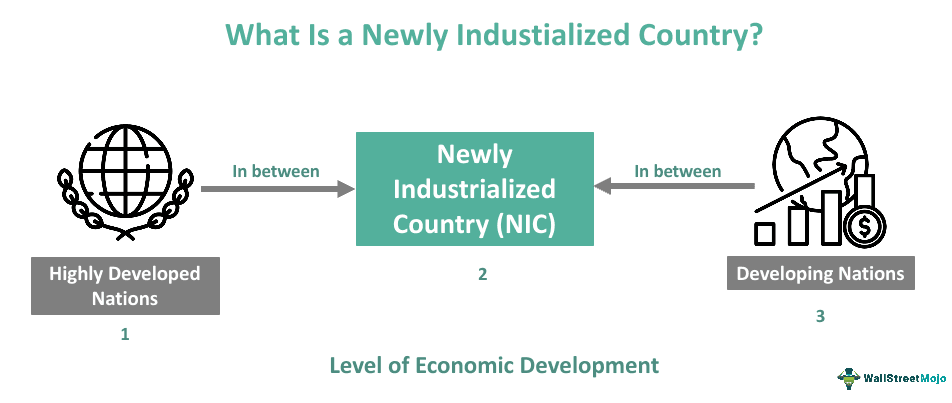

A Newly Industrialized Country (NIC) refers to a group of nations that fall between developing and advanced developed countries. The primary goal of NICs is to stimulate economic growth and advance the development of their economies. Therefore, these countries are often called "advanced developing" countries.

NICs gained prominence in the late 20th century as certain nations shifted from primarily agricultural economies to those driven by manufacturing or the service sector. This transition significantly influenced global economic growth patterns. In recent years, several Asian nations have emerged as prominent examples of NICs, showcasing rapid industrialization and economic advancement.

- Newly Industrialized Country (NIC) consists of nations that have witnessed a shift from agricultural to manufacturing or service sector.

- They aim to earn revenue through foreign investments and exports. The government also encourages development and schemes to boost economic growth.

- The origin of this concept arose between the 1970s and 1980s. Initially, Asian Tigers consisting of South Korea, Hong Kong, Taiwan, and Singapore were a part of it.

- The NICs include India, Brazil, Mexico, China, Thailand, South Africa, Taiwan, Singapore, Turkey, and Hong Kong.

Newly Industrialized Country Explained

The newly industrialized country category consists of nations that have seen a vital transition from primary occupation to the tertiary sector. They aim to develop these nations into a more urbanized and industrialized economy. Since the 1970s, most nations have been a part of it. A few of them in the newly industrialized country list include Hong Kong, Singapore, South Korea, and Taiwan, collectively known as Asian Tigers. These nations predominantly excelled in industrialization and growth during the 1970-1980s.As a result, these countries became highly competitive in technology and innovation, leading to a focus on boosting their GDP through exports. Additionally, workers were moved significantly from rural to urban areas to support industrial development. However, in the later stages, other nations also joined the cause.

Understanding the historical background is crucial to grasp the beginnings of this change. The roots of industrialization can be traced back to the Industrial Revolution, which many nations had already embraced. However, during the late 1700s and 1800s, British colonial rulers established colonies and exploited less developed countries, causing significant disparities. Consequently, resources were extracted from these nations, leaving them impoverished and hindering their overall growth.

Nonetheless, specific factors played a pivotal role in driving the growth of newly industrialized countries. Government intervention in the economy emerged as a crucial catalyst for economic development in NICs. Governments implemented policies encouraging business participation and amending existing regulations to facilitate growth and progress.

Characteristics

Let us look at the characteristics of newly industrialized country growth to comprehend the concept better:- NICs usually have a shift from agriculture to the manufacturing sector, which becomes a significant contributor to their GDP.

- These nations receive huge capital investments via FDI (Foreign Direct Investments).

- There is a tremendous boost in the exports sector.

- NICs often recover significantly, transitioning from negative GDP growth rates to positive values.

- Governments in NICs play an active role in promoting production and innovation.

- Better civic amenities like good transportation, water, and electricity are provided to the public.

- The laws and regulations within the economy are improvised for the betterment of society.

Newly Industrialized Country - Definition, Characteristics, Examples

Guide to Newly Industrialized Country and its definition. We explain its characteristics, examples, and comparison with developed nations.

Newly Industrialized Country - Definition, Characteristics, Examples

Guide to Newly Industrialized Country and its definition. We explain its characteristics, examples, and comparison with developed nations.

")