Pakistan has quietly executed one of the most significant shifts in its energy strategy over the past five years. We should name it for what it is:

a success.

Not a partial success. Not a success-in-progress. But a structural achievement that has fundamentally altered the country’s exposure to the two greatest threats to energy security: (1) Strait of Hormuz blockade, and (2) economic coercion via expensive fuel contracts.

The fact that this transformation has gone largely unnoticed in policy circles is itself revealing. Pakistan’s energy system was architected for crisis five years ago. Today, it is architected for resilience. And the mechanism is worth understanding—not because it’s complex, but because it’s instructive.

The Crisis: One-Third of Supply at Risk

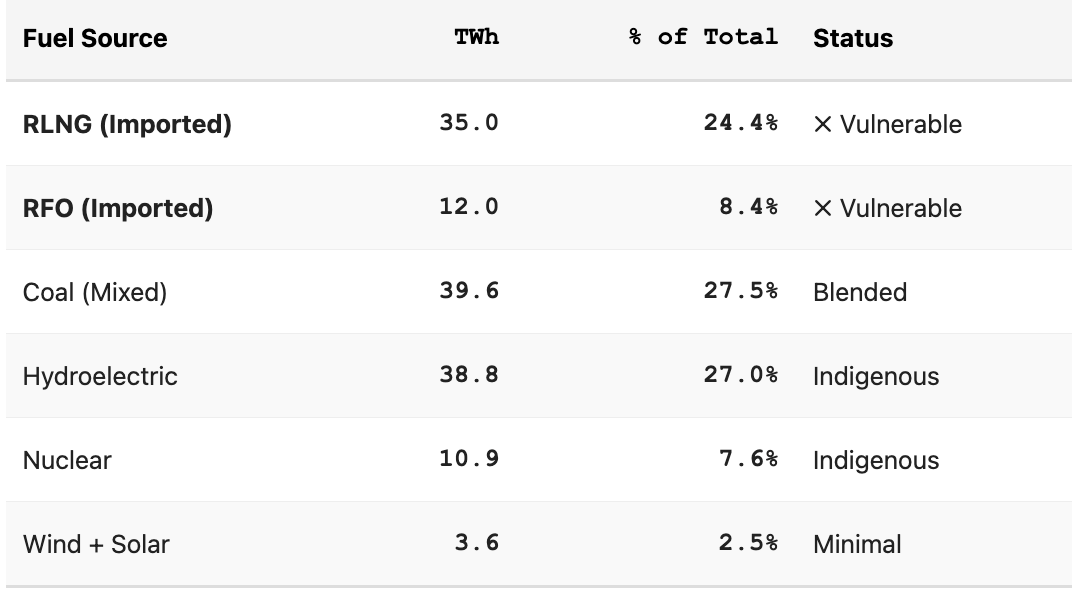

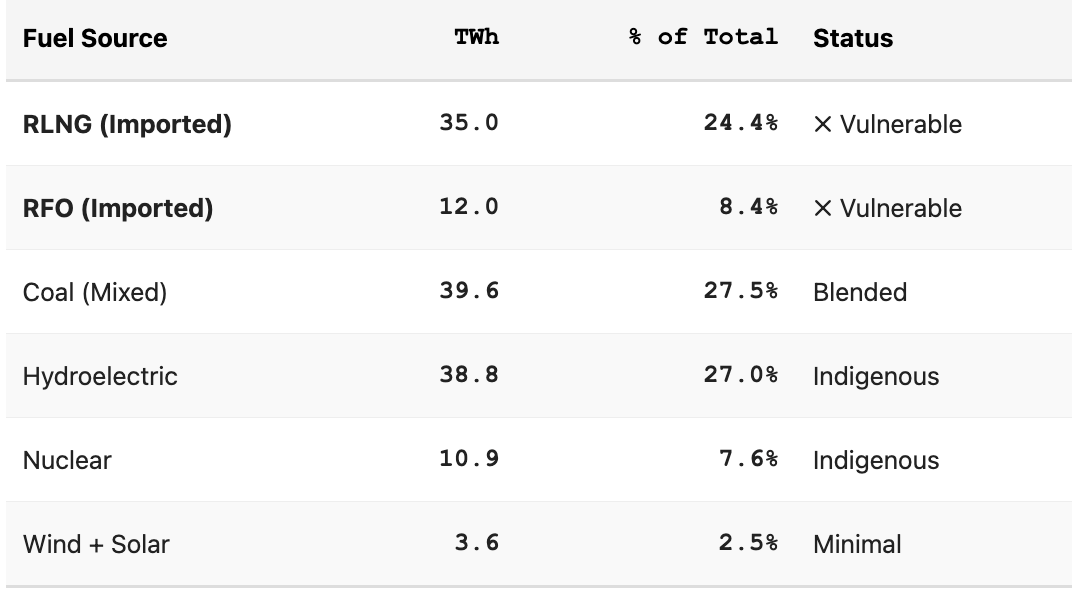

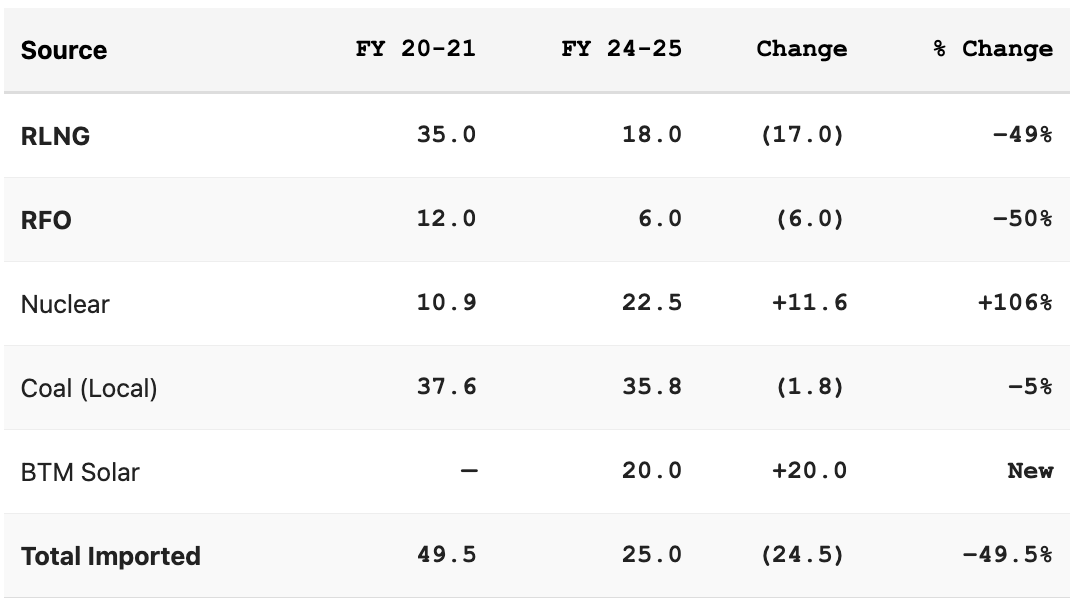

In FY 2020-21, Pakistan’s power system rested on a precarious foundation. Consider the arithmetic:

Total imported fuels: 49.5 TWh (one-third of supply). This was not a stable energy base. A thirty-day blockade of the Strait of Hormuz—through which 90% of global seaborne oil and our LNG cargoes flow, would have cost the system

2.87 TWh, enough to trigger cascading load-shedding of greater than

eight hours daily and demand destruction.

“The system was not designed for this risk; it merely accepted it as the cost of energy growth.”

The Shift: Five-Year Transformation

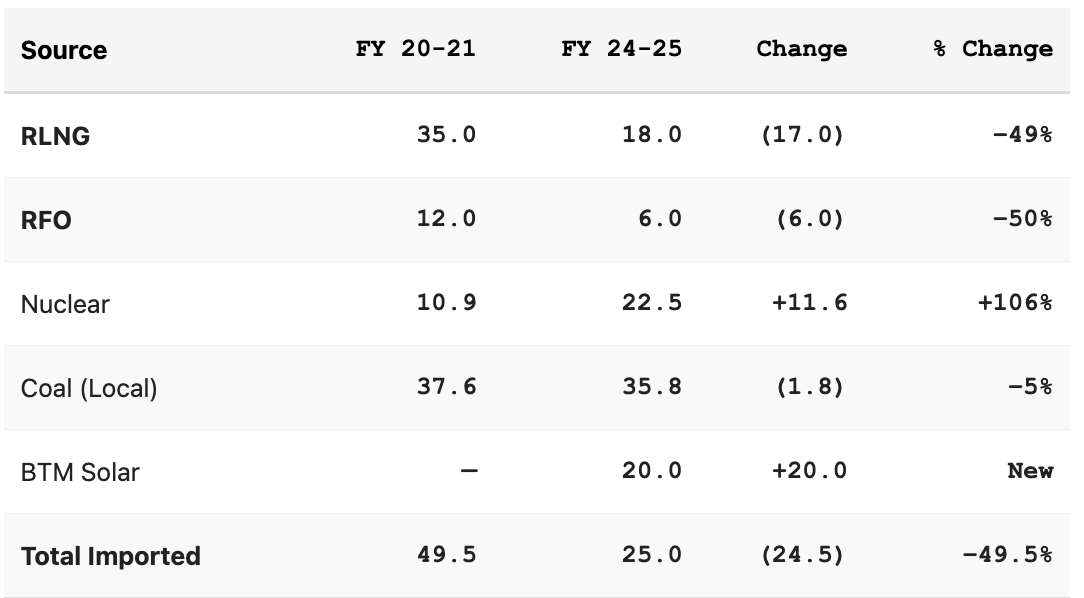

By FY 2024-25, the arithmetic has fundamentally changed:

How It Happened: Three Pillars

The transition was not accidental. It resulted from three moving parts that operated in sequence, each enabling the next.

Pillar 1: Nuclear Baseload (Policy-Driven)

K-2 reactor, commissioned May 2021, added 1,145 MW of capacity. Nuclear generation more than doubled: from 10.9 TWh (FY 2020-21) to 22.5 TWh (FY 2023-24, +106%). This was not marginal. A 1,100 MW baseload plant running at 95% capacity factor produces 9 TWh annually—enough to displace 9 TWh of expensive RLNG.

The mechanism is straightforward: RLNG plants can be throttled back without grid instability when nuclear baseload provides the foundation. K-2 was designed precisely for this. The policy worked.

https://substackcdn.com/image/fetch...c859-6e97-459c-b843-8b775fb561ec_1084x266.png

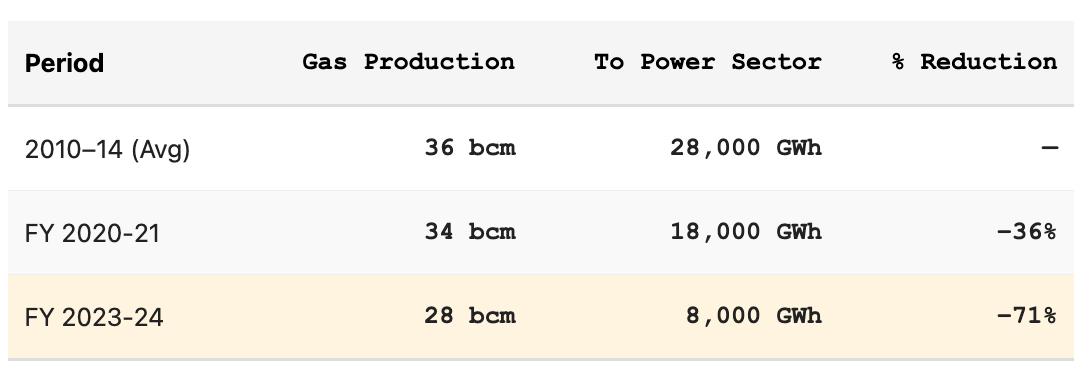

Pillar 2: Coal Stabilization (Structural Recovery)

This is where the mechanism becomes visible. Pakistan has proven coal reserves of 175 billion tonnes in Thar, Sindh. Yet coal-based generation hovered around 37 TWh for a decade. The issue was not resource availability but

dispatch economics.

RLNG was being forced to run (due to take-or-pay contracts with Qatar) even when coal was cheaper:

https://substackcdn.com/image/fetch...624a-31f1-48db-938a-55601e4535a0_1084x352.png

Pakistan was paying a Rs 12/kWh premium to run expensive imported fuel rather than cheaper coal sitting in the ground.

As RLNG volumes contracted (from 35 to 18 TWh), coal regained its position in merit order. By FY 2024-25, coal generation stabilized at 35.8 TWh. This is not growth—it is durability. The structure shifted; coal became the swing fuel.

Pillar 3: Behind-the-Meter Solar (Market-Driven)

And here is where the story becomes fascinating. Between 2022 and 2024, Pakistan imported 24-31 GW of solar modules. Only 4 GW went to utility-scale IPPs.

The remaining 20-27 GW went onto factory roofs, agricultural fields, and residential terraces.

By mid-2025, Pakistan had accumulated 14-20 GW of BTM solar capacity, generating an estimated 20 TWh annually—generation that never passes through a DISCO meter, never appears in national statistics, yet is entirely indigenous.

The economic mechanism was simple: DISCO tariffs climbed to 30+ Rs/kWh. Payback periods for rooftop solar fell to 3-4 years. Rational actors—factories, farms, middle-class households—responded by investing in solar and exiting the grid.

The decentralized revolution was bottom-up, not policy-driven.

https://substackcdn.com/image/fetch...9d69-40ad-45f7-85d5-aec313b0eb5a_1084x278.png

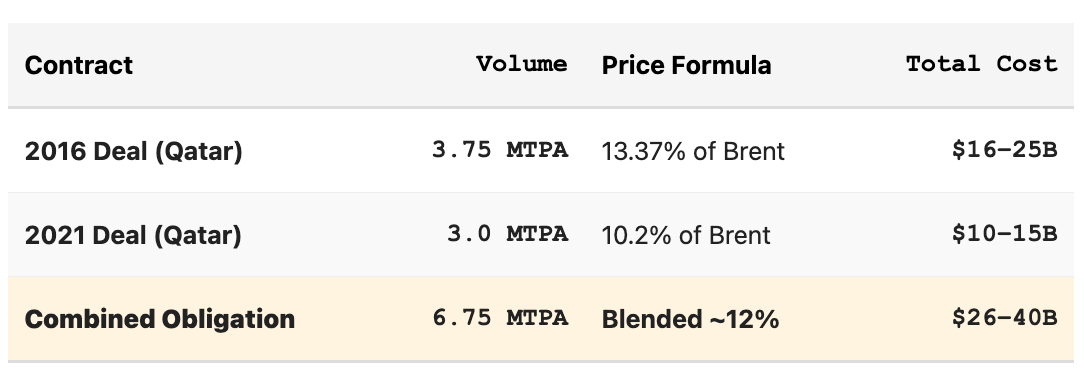

The Hidden Crisis: Economic Lock-In Broken

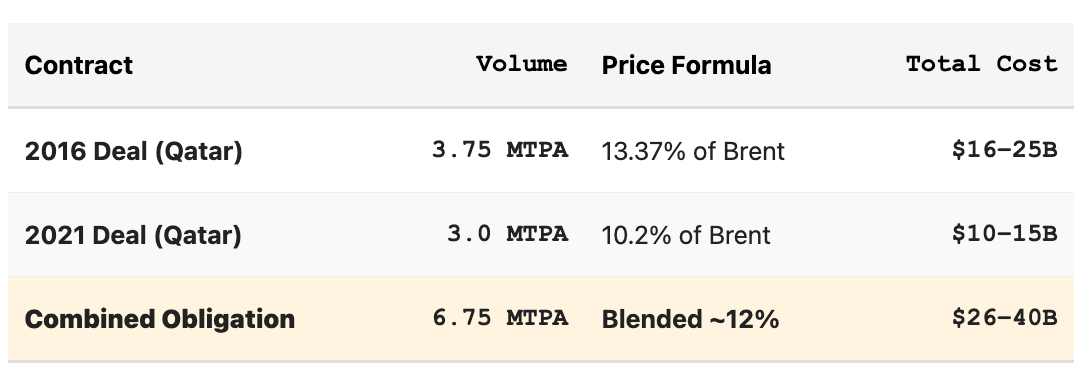

Behind the geopolitical story lies a deeper economic one. Pakistan signed two long-term contracts with Qatar backed by take-or-pay sovereign guarantees:

Under take-or-pay clauses, Pakistan was obligated to pay for contracted volumes

regardless of actual demand. This created a financial trap: even if demand fell (due to economic recession, solar adoption, or cheaper coal), Pakistan was obligated to pay.

The Cost of Forced Running

Annual excess cost (FY 2022-23): Rs 9,408 billion (~$32M USD) in forced RLNG premium vs. optimal coal/gas dispatch.

5-year cumulative economic waste: Rs 37–47 trillion ($125–160B USD). This was a hidden tax on consumers passed through tariffs.

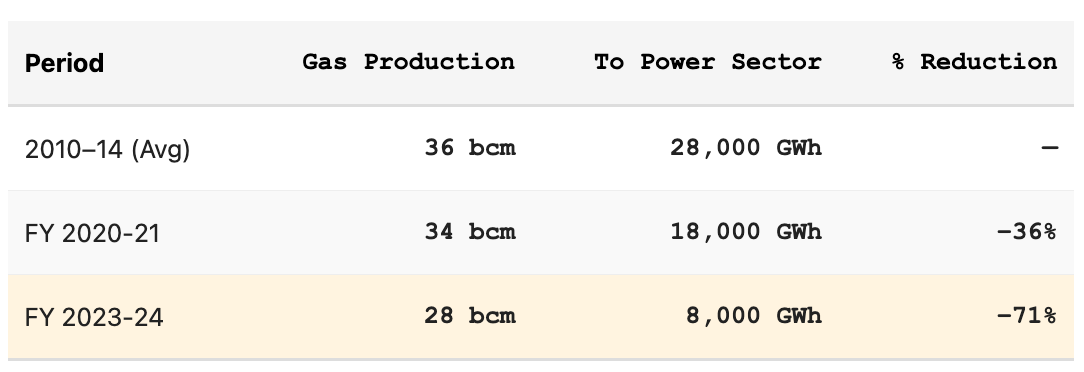

Pakistan was also actively suppressing its own domestic gas:

Petroleum Minister Ali Pervaiz Malik stated it explicitly:

“Domestic gas producers are unable to sell gas to the power sector because regasified LNG plants are forced to run to absorb contractual supplies.” This is perverse: Pakistan was starving its own domestic gas sector while being forced to buy expensive imported LNG.

By reducing RLNG from 35 to 18 TWh, Pakistan freed up pipeline capacity for domestic gas and allowed coal to reclaim merit order. The economic stranglehold was released.

The Geopolitical Victory

Now, consider the blockade scenario. If the Strait of Hormuz were blocked for 30 days today, Pakistan would lose 1.46 TWh of RLNG generation. The policy response would be straightforward

https://substackcdn.com/image/fetch...8cd6-55a1-464d-9a63-fb080e57d6fc_1084x372.png

This is manageable. Five years ago, the same blockade would have cost 2.87 TWh, a crisis-scale event requiring emergency external intervention. The difference is not marginal; it is the difference between a manageable shock and a systemic crisis.

More interesting still: a Strait blockade today would actually unlock economic potential. The power sector could absorb an additional 4-5 TWh of domestic gas without infrastructure expansion. Imported coal imports (currently minimal at 0.5 TWh) could be halted entirely, shifting to full domestic coal capacity. The system would not break;

it would reconfigure toward indigenous resources.

This is the architecture of energy security. It is not built on goodwill or geopolitical alignment; it is built on the structure of the energy system itself.

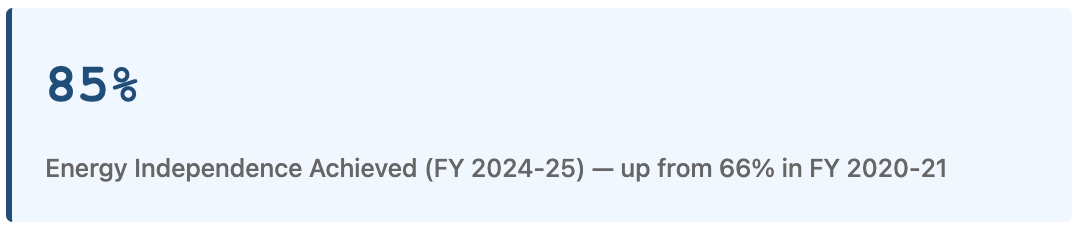

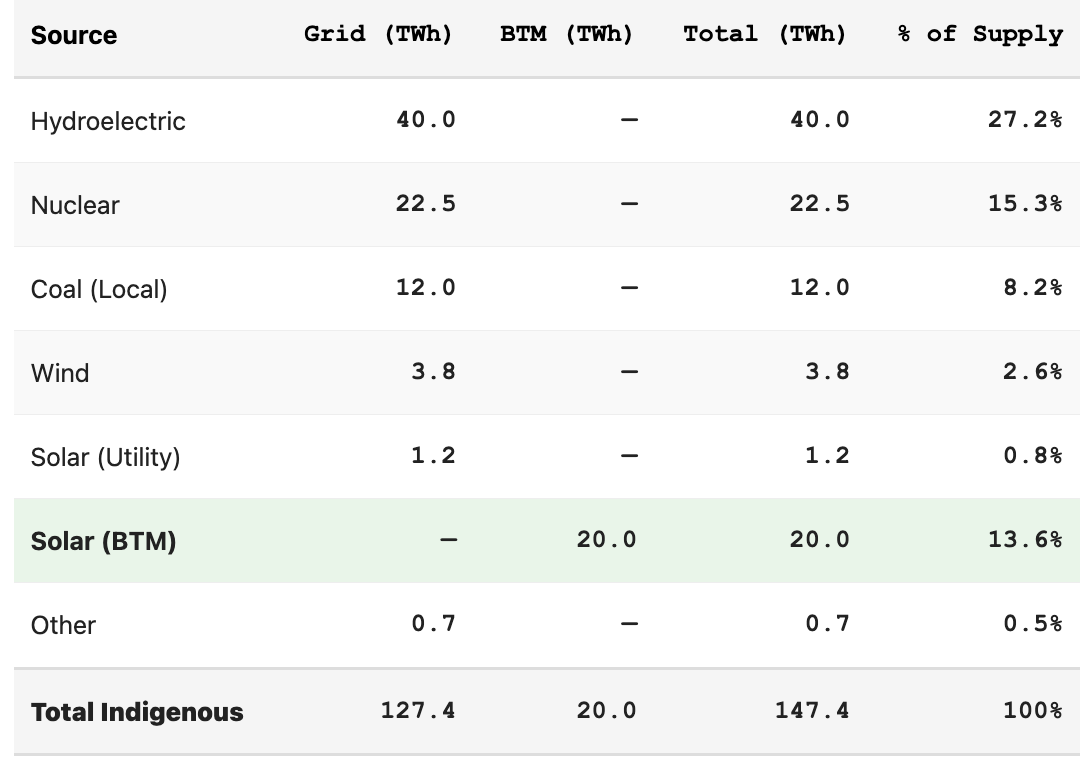

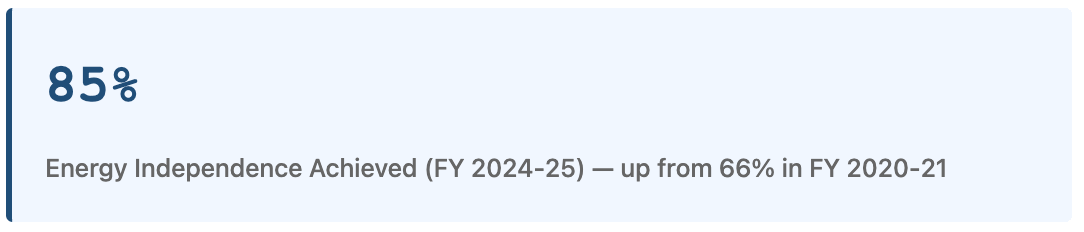

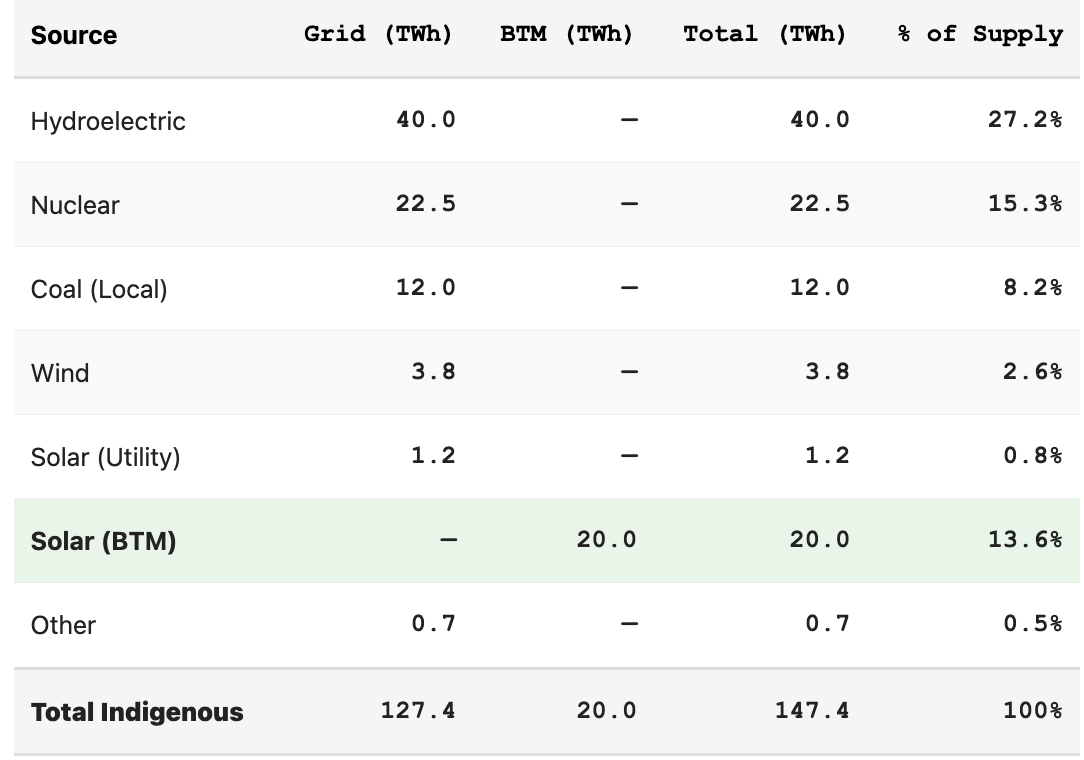

The Total Picture: 147 TWh Indigenous

When you add grid generation (127.4 TWh) to BTM solar (20 TWh), Pakistan now generates 147.4 TWh of total indigenous power. Only 25 TWh is imported.

Energy independence: 85% (up from 66%). All actual electricity consumption is met by domestic sources: hydropower, nuclear, local coal, wind, solar (utility + BTM), and renewables. Imported fuel dependency has been nearly eliminated except for marginal RLNG/RFO for peak shaving.

The Six Insights You Need

https://substackcdn.com/image/fetch...d7e-cb04-4606-86e8-b2eb9ec77064_1084x1592.png

What Comes Next

Pakistan has (almost) solved the energy security problem. The remaining agenda is operational efficiency, tariff restructuring, and economic reform:

Renegotiate Contracts

At 18 TWh RLNG (vs 35 TWh baseline), Pakistan is now a marginal buyer, not a strategic asset. Leverage exists for 2026 renegotiation.

Formalize BTM Solar

Bring 20 TWh into official accounting. Enable net metering for BTM, and make buyback price market competitive, rather than rigid, and fixed. Dynamic pricing and time-of-use tariffs required to prevent hidden cross-subsidies.

Two-Part Tariff

Move from a variable-pricing based tariff to a tariff that transparently recovers fixed cost, and sells energy at the margin. This changes the way energy economics work in the country

Five years ago, Pakistan’s energy system was architected for crisis. Expensive imported fuels dominated. Blockade risk was existential. Economic lock-in strangled the economy. Demand was being destroyed by tariff spirals.

Today, it is architected for resilience. Indigenous sources dominate. Blockade risk is halved. Economic trap is broken. Demand can be managed through efficiency, not crisis suppression.

The fact that this success has gone largely unnoticed says something about how policy circles think about energy. We celebrate projects. We debate tariffs. We argue over subsidies. But structural transformation, the kind that rewires the entire system, often happens quietly, in the margins, through the accumulated decisions of millions of actors (nuclear plants, coal miners, solar installers, farmers) responding to incentives.

That is what Pakistan has achieved.

open for business

open for business