Fitch Affirms Indonesia at 'BBB'; Outlook Stable

Tue 11 Mar, 2025 - 04.47 ET

Fitch Ratings - Hong Kong - 11 Mar 2025: Fitch Ratings has affirmed Indonesia's Long-Term Foreign-Currency Issuer Default Rating (IDR) at 'BBB' with a Stable Outlook.

A full list of rating actions is below.

Key Rating Drivers

Credit Strengths and Weaknesses: Indonesia's 'BBB' rating reflects the country's favourable medium-term growth outlook and low government debt/GDP ratio. The rating is primarily constrained by a weak government revenue intake and lagging structural features, such as GDP per capita and governance indicators compared with 'BBB' category peers.

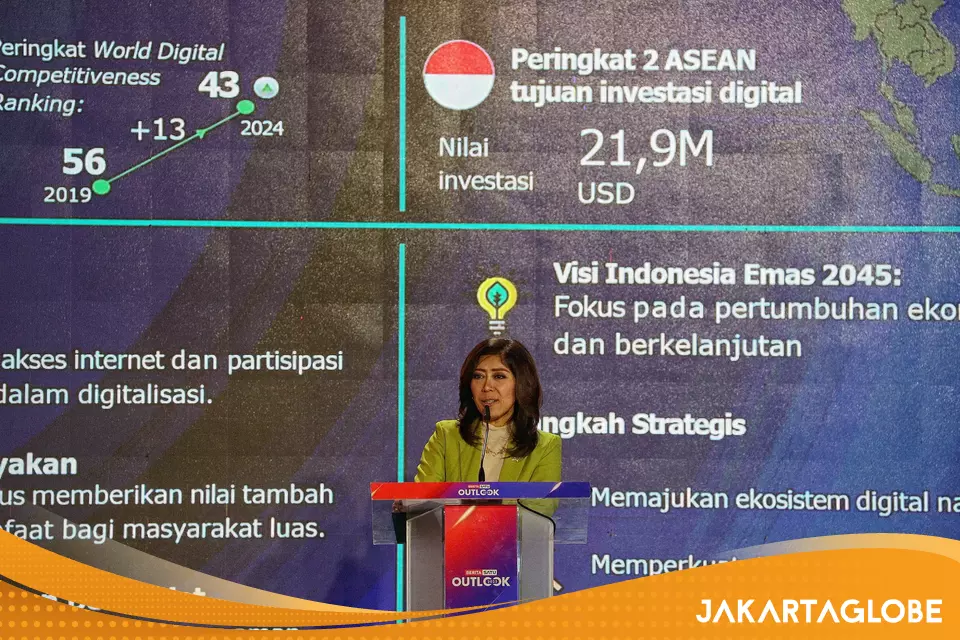

Resilient Growth Outlook: Fitch forecasts Indonesia's real GDP to grow by 5.0% in 2025, maintaining momentum from 2024 and outperforming many 'BBB' category peers (median: 3.3%). Strong domestic demand, supported by public spending on social assistance and infrastructure projects, will be the main growth driver. Private investment should remain robust, driven by modest monetary policy easing, reduced policy uncertainty post-elections and continued downstreaming activities.

Potential External Headwinds: We forecast growth to ease slightly to 4.9% in 2026 as higher US tariffs and weaker demand from China exert more pressure on Indonesia's exports, although resilient domestic demand should mitigate some of the pressures.

Challenging Growth Targets: The government aims for 8% growth by 2029 while maintaining economic stability, including through continued prudent fiscal policies. This target looks challenging without significant structural reforms. The key policy agenda thus far includes a free meals programme and initiatives for food and energy self-sufficiency. It also includes investment via the newly launched Danantara sovereign wealth fund (SWF), commodity downstreaming and expanded electric-vehicle and battery manufacturing.

Modest Inflationary Pressure: The headline CPI fell for the first time in over two decades by 0.1% yoy in February 2025, on temporary discounts on household electricity tariff, while core inflation held steady at 2.5% yoy. We project headline CPI to rise to 2.7% by end-2025 as discounts diminish and food prices increase, staying within the current official inflation target band at 2.5% +/- 1pp. We expect the Bank Indonesia to further cut the policy rate by 50bp to 5.25% by end-2025, following a 25bp cut in January.

Fiscal Uncertainty: We project the fiscal deficit to rise to 2.5% of GDP in 2025, up from 2.3% in 2024. However, the fiscal outlook is highly uncertain, particularly over the medium term. Reversing the planned 1pp VAT rate increase would result in a Fitch-estimated revenue loss of 0.3% of GDP. The government's efforts to enhance spending efficiency, including 1.3% of GDP in spending cuts reallocated to the free meals programme, may face challenges in fully using the budget savings, potentially leading to underspending.

Government Debt Ratio to Decline: Fitch forecasts a moderate decline in general government debt to 39.1% of GDP in 2028 from 40.4% in 2025 (BBB median: 58.0%). We expect a mild increase in the budget deficit over the coming years to accommodate the government's additional public social spending and infrastructure investment. This reflects our baseline assumption that the government, supported by a broad parliamentary coalition, will continue to adhere to the deficit ceiling of 3% of GDP in the medium term.

New SWF: The recent passage of Indonesia's new SOE law paved the way for the establishment of Danantara SWF on 24 February 2025. The government plans to consolidate its state-owned enterprise (SOE) portfolio under this new investment vehicle. The initial plan involves channelling funds from budget savings and SOE dividend payments to finance prioritised national projects, such as downstream industries, renewable energy, food production, affordable housing and AI.

Danantara's investment strategy is still unclear. Even so, borrowing through Danantara or SOEs under it may increase contingent liability risks to the sovereign balance sheet. Public nonfinancial corporation gross debt accounted for roughly 5% of GDP in 2024, according to the official source.

Low Revenue Intake: We project the general government revenue/GDP ratio to average 14.3% during 2025 and 2026, well below the 'BBB' category peer median of 21.2%. This reflects our expectation of falling commodity prices and challenges in meaningfully raising revenue in the coming years, especially after reversing the planned VAT rate hike. Persistently low revenue intake also contributes to Indonesia's high interest/revenue ratio, which we project at 15.6% in 2026, against the 'BBB' peer median of 8.4%.

CAD to Widen Further: We forecast the current account deficit to widen to 1.3% of GDP in 2025, up from an estimated 0.6% in 2024. We expect weaker global demand, rising trade protectionism and declining commodity prices to reduce Indonesia's goods trade surplus. We expect the basic balance, including current account and net FDI, to revert to a deficit in 2025, moderately increasing dependence on volatile portfolio flows. Non-resident holdings of local-currency government debt are likely to remain well below pre-Covid-19 levels.

Rise in FX Reserves: Indonesia's foreign exchange (FX) reserves increased by 7.3% yoy to USD154.5 billion in February 2025, equivalent to about 5.6 months of current-account payments. This was broadly in line with the 'BBB' median level.

The government recently issued a regulation on FX retention that requires natural resource exporters to deposit 100% of FX earnings into a special account at national banks for 12 months, in a bid to support currency stability and contain market volatility. However, Indonesia's external liquidity - measured by the ratio of liquid external assets to liquid external liabilities - remains weaker than many 'BBB' peers.

ESG - Governance: Indonesia has an ESG Relevance Score (RS) of '5' and '5[+]' respectively for both Political Stability and Rights and for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption. These scores reflect the high weight that the World Bank Governance Indicators (WBGI) have in our proprietary Sovereign Rating Model.

Indonesia has a medium WBGI ranking at 49th percentile, reflecting a recent record of peaceful political transitions, a moderate level of rights for participation in the political process, moderate institutional capacity, established rule of law and a high level of corruption.

RATING SENSITIVITIES

Factors that Could, Individually or Collectively, Lead to Negative Rating Action/Downgrade

- Public Finances: A material increase in the overall public debt burden closer to the level of 'BBB' category peers, resulting, for example, from a substantial rise in fiscal deficits, or materialisation of contingent liabilities.

- External Finances: A sustained decline in FX reserve buffers, resulting, for example, from outflows stemming from deterioration in investor confidence or large FX interventions.

Factors that Could, Individually or Collectively, Lead to Positive Rating Action/Upgrade

- Public Finances: A marked improvement in the government revenue ratio closer to the level of 'BBB' category peers, including from better tax compliance or a broader tax base, which would strengthen public finance flexibility.

- External Finances: A material reduction in external vulnerabilities, for instance, through a sustained increase in FX reserves or lower exposure to commodity price volatility.

- Structural: Significant improvement in structural indicators, such as governance standards, closer to those of 'BBB' category peers.

Moodys

Find the latest ratings, reports, data, and analytics on Indonesia,Sovereign & Supranational

www.moodys.com

Credit rating agencies warn that a downgrade could be on the horizon if the government struggles to sustain economic growth or allows the fiscal deficit to widen by prioritizing political commitments over prudent financial management.

www.thejakartapost.com