Indonesia's tightening coal policy begins to reshape export flows

6 Mar 2026

- Indonesia's coal production and exports fall in 2025 on lower demand from China, India

- Indonesia considering cutting coal output to around 600 mnt, tightening export availability

- Middle East tensions are pushing up freight costs, landed prices for Asian buyers

Morning Brief: Indonesia's coal production and exports fell in 2025 on lower demand from China and India. Indonesia is considering cutting coal output to around 600 million tonnes, tightening export availability Middle East tensions are pushing up freight costs, lifting landed coal prices for Asian buyers

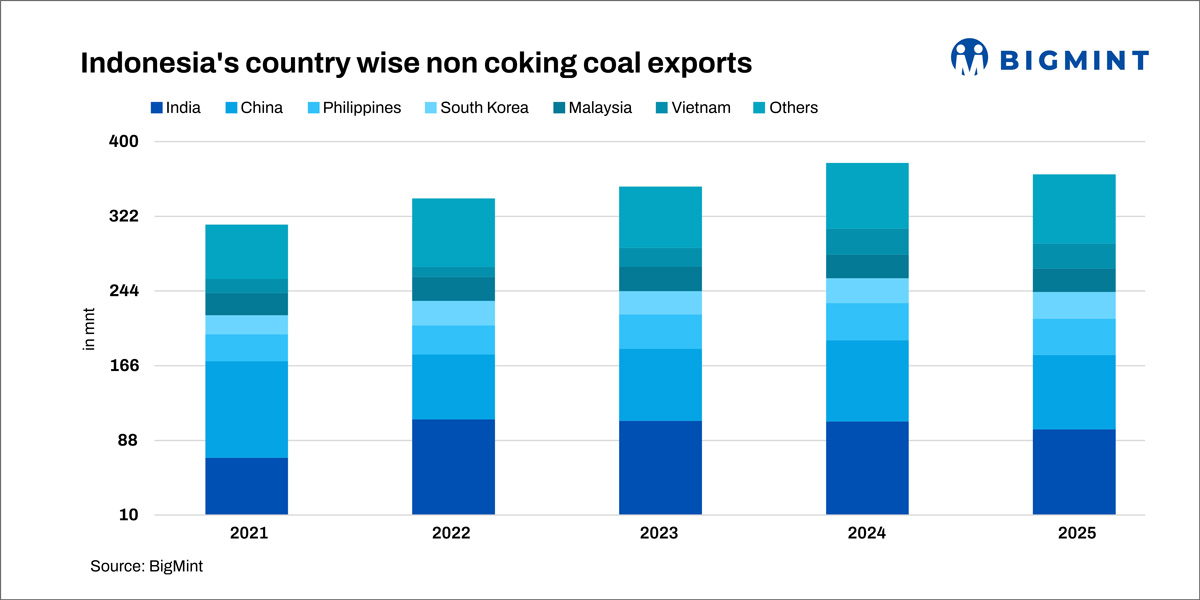

India typically imports around 160-170 million tonnes of thermal coal each year, with roughly 100 million tonnes sourced from Indonesia, making it the dominant supplier of the low-calorific coal used by Indian coastal power plants.

Indonesia is now moving toward tighter control of coal production, exports and pricing. For India, which relies heavily on Indonesian low-CV material, the shift has direct implications for supply availability and price formation.

Production slowdown and policy tightening

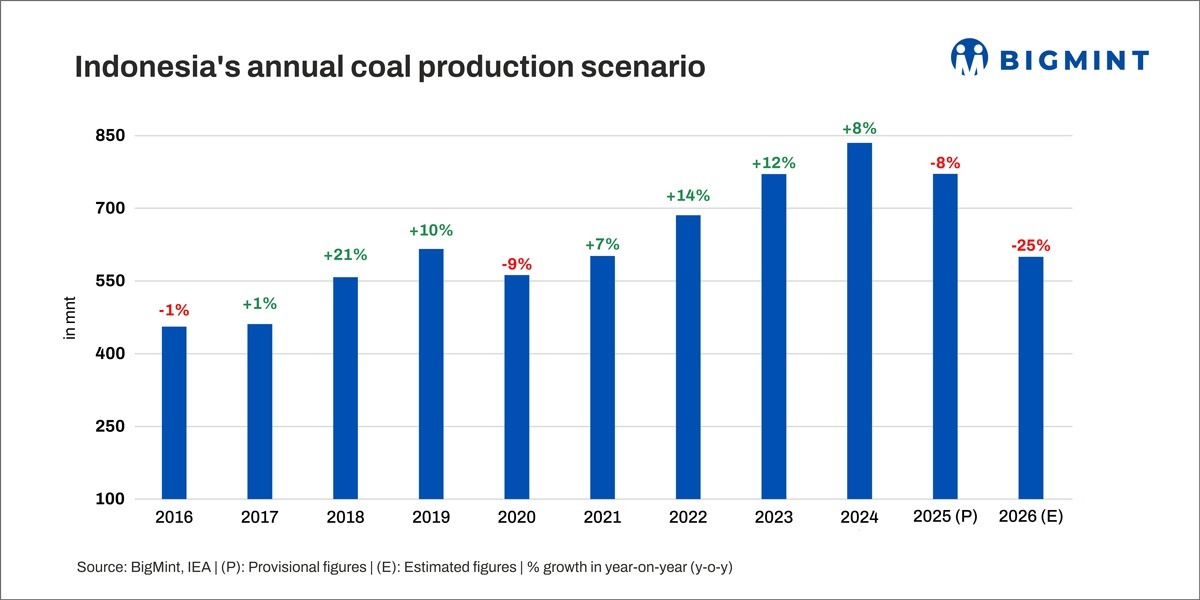

The policy recalibration follows a softer year for Indonesia's coal sector. The country's coal production stood in the range of 750-790 million tonnes in 2025, down 5.5% from a year earlier, while exports declined 6% to about 533 million tonnes. Market participants estimate that production could drop 25% during the year, reflecting adjustments by miners as demand weakened.

The drop marked the first decline in both production and exports since 2020, when the Covid-19 pandemic disrupted demand and supply chains. Weaker demand from China and India contributed to the slowdown as both countries increased domestic coal availability while renewable generation expanded, reducing import requirements.

Against this backdrop, Jakarta has begun tightening oversight of production through stricter approvals under the RKAB system, formally known as Rencana Kerja dan Anggaran Biaya. The RKAB is the annual work plan and budget that mining companies must submit to the government outlining their planned production levels, operational activities and expenditure for the coming year. Industry participants say the government is considering reducing the production envelope to around 600 million tonnes.

Ramli Syed Ahmad, president director of PT Ombilin Energi, described the potential reduction as substantial, noting that it would represent close to a 25% cut, equivalent to roughly 200 million tonnes of output.

"The move to tighten RKAB approvals appears aimed at supporting coal prices, though it may not be sustainable if demand remains weak," said Ramli Syed Ahmad, president director of PT Ombilin Energi.

The policy shift has introduced uncertainty for producers and buyers. Ahmad explained that many miners had already planned equipment purchases and capital expenditure after receiving three-year RKAB approvals covering 2024 to 2026. The governments decision to reassess the 2026 approvals forced companies to revisit their production plans.

In the early months of the year, some miners were allowed to produce only a quarter of their previously approved volumes while waiting for new approvals, temporarily constraining export availability.

Implications for Indian buyers

The tightening reflects a broader policy objective to stabilise prices, manage oversupply and prioritise domestic energy security. Indonesia requires miners to sell at least 25% of their production locally under the country's domestic market obligation (DMO) rules.

Domestic coal sales reached about 254 million tonnes in 2025, while year-end stockpiles stood at roughly 22 million tonnes. Authorities have indicated that DMO requirements will be prioritised before determining how much coal can be allocated for exports.

Indonesia has also introduced additional regulatory measures to tighten market conditions and strengthen oversight. These include reverting to annual RKAB approvals, tightening compliance rules on mine reclamation, adjusting domestic benchmark prices under the HBA system, and considering fiscal measures such as potential export duties.

For international markets, the practical effect is a more managed export pipeline. When production quotas tighten, miners typically prioritise long-term contractual deliveries, leaving fewer cargoes available in the spot market. Spot availability becomes more volatile, with prices responding quickly to changes in export supply.

India sits directly in the path of these shifts. The country sources a large share of its imported thermal coal from Indonesia, particularly the low-calorific grades used by coastal utilities and certain industrial consumers designed to operate on these specifications.

Rajat Handa, vice president for international trade at Agarwal Coal Corporation, said India's total coal imports are likely to remain around 150-160 million tonnes annually, with roughly 95100 million tonnes coming from Indonesia because it remains the most competitive supplier of low-CV coal.

However, Handa noted that India's dependence does not mean buyers lack flexibility. If Indonesian prices move beyond acceptable levels, Indian utilities and traders can shift procurement to alternative suppliers such as Russia, Australia or South Africa.

That possibility concerns some Indonesian producers. Ahmed warned that once buyers establish alternative supply relationships, it can be difficult for Indonesian exporters to win them back. New suppliers often offer attractive long-term contracts, gradually eroding Indonesias dominance in the low-CV coal trade.

Outlook

Geopolitical tensions are also beginning to influence market dynamics. Escalation of conflict in the Middle East has raised freight and energy costs across global commodity markets, increasing bunker fuel prices and shipping risks along key maritime routes. For Asian coal importers, this translates into higher landed costs even when FOB coal prices remain relatively subdued.

In the near term, Indonesias policy shift has already lent a firmer tone to the market. Indian port prices have risen modestly as buyers respond to uncertainty surrounding production approvals and export availability.

Indian portside prices for Indonesian-origin thermal coal increased sharply w-o-w on 03 March 2026, supported by tight supply and geopolitical tensions between the United States and Iran, which have injected uncertainty into global energy markets. According to BigMint's latest assessment, 5,000 GAR coal prices rose by INR 450/t w-o-w, reaching INR 8,800/t at Kandla and INR 8,700/t at Vizag. The 4,200 GAR segment also registered a similar increase of INR 600/t, with prices climbing to INR 7,100/t at Kandla and INR 7,000/t at Vizag.

Over the longer term, the outcome will depend on how consistently Indonesia manages its regulatory framework. The country remains the largest supplier in the seaborne thermal coal market. But as the government moves toward tighter production governance and stronger domestic prioritisation, the reliability of Indonesian exports may become an increasingly important consideration for import-dependent markets such as India.

Indonesia's coal production and exports fall in 2025 on lower demand from China, India Indonesia considering cutting coal output to around 600 mnt, tighte

www.bigmint.co